The latest annual report from the International Energy Agency (IEA) confirmed that the world is not investing enough to meet its future energy needs. Importantly, this is true for both low-carbon energy and fossil fuels. And ironically enough, the oil and gas industries are today among the only ones whose investments are reasonably in line with the objectives of the 2050 carbon neutrality scenario. Good news? Not so sure. If demand (estimated to rise for at least 10 to 15 years) is stronger than supply, it is likely that a new oil or gas shock will take place. This hypothesis was already discussed in the 2018 IEA report, the pandemic has only accentuated its probability and possible consequences [1].

On a longer-term perspective, another aggravating factor adds to this picture: the exponential growth of the energy needed to produce hydrocarbons. Let's go back to the basics: all energy production requires an initial energy input, which can be estimated for each stage of the production chain. This energy can include direct energy costs (e.g. oil burned to pump petroleum), indirect energy costs (e.g. materials embedded energy), and even more (the energy used by employees to work on site, by the government to monitor companies, etc.). The ratio of the energy produced over the energy required for production is called the "energy return on investment" (EROI) and is generally established either right after production (this is called the standard ERO) or at the final-consumer level.

For oil and gas, the evolution of EROIs over the long-term (past and future) has been little discussed, even though these two energy sources still account for more than half of the world's primary energy production. Two recently published studies have sought to fill this gap by quantifying the EROI of both fuels production (i.e. without including refining or distribution) from 1950 to 2050 [2][3].

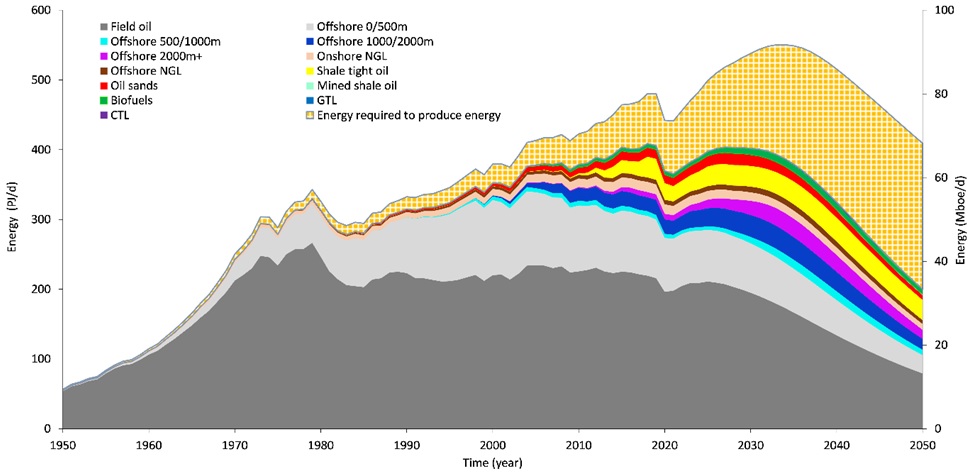

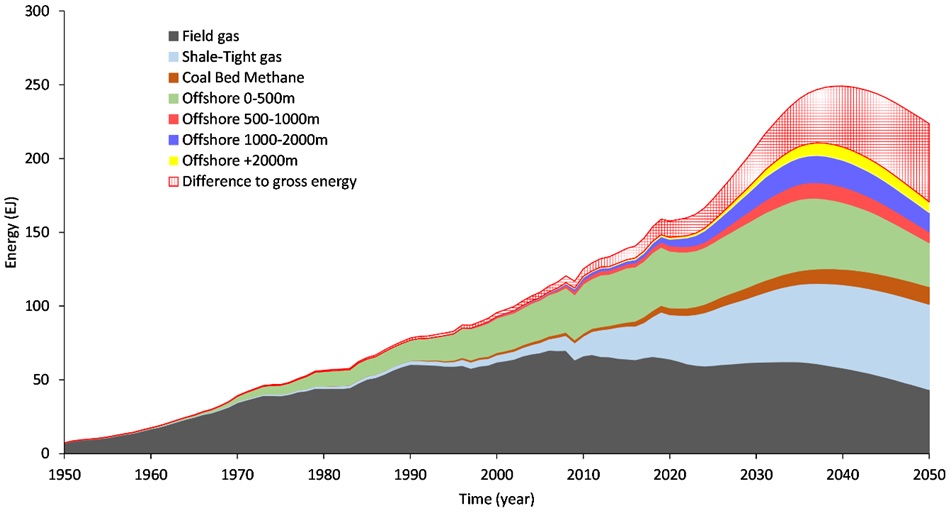

They estimate that the energy required to produce all oil liquids today is equivalent to 16% of that same production (Figure 1). Because of the human preference to exploit the easiest resources first (so-called conventional), this energy should grow at an exponential rate: by 2050, a proportion equivalent to half of the gross energy production will be necessary. For gas, the authors estimate that the energy needed for production is equivalent to 7% of the gross energy produced today, and 24% by 2050 (Figure 2). By way of comparison, the energy currently required for hydrocarbon production (oil liquids and gas) is equivalent to the combined primary energy consumption of France, the UK, Germany and Italy. Two issues are highlighted by the authors.

Figure 1: Average oil liquids net-energy production from 1950 to 2050,

compared to the gross energy. Click the image to enlarge.

Figure 2: Average gas net-energy production from 1950 to 2050,

compared to the gross energy. Click the image to enlarge.

First, a decrease in the standard EROI results in an increase in energy consumption by the energy production sector, a phenomenon also known as "energy cannibalism." Since all energy production affects the environment, an exponential decrease in EROI suggests an acceleration of environmental damage by this sector.

Second, the energy transition implies a decrease in the standard EROI, and possibly the societal EROI [4]. In other words, a reduction in the energy available for society's other needs is likely, unless we imagine a dramatic increase in primary energy production if it is not accompanied by a major effort in energy sobriety, which is difficult to achieve in view of recent developments on this front. In the current state of projections, this decrease may have significant economic effects: decrease in asset prices, recession, stagnation, stagflation, and growing inequalities [5].

A potential bottleneck is emerging: fossil fuels maintain cheap energy abundance and thus sustain global economic growth. Their climatic, social and environmental impacts are pushing us towards their abandonment in favor of low-carbon energy sources, requiring a significant energy, material and economic input. Due to a lack of investment, an oil or gas shock is likely in the next few years and could lead to a significant economic crisis in the context of an already fragile post-pandemic recovery. The energy transition would be all the more difficult and the use of fossil fuels to boost economic growth, which is possible to a certain extent but environmentally and socially risky, represents a major concern. This is especially true for coal, which is the fossil fuel with the highest EROI, the largest reserves, and the heaviest climate and environmental impacts.

In conclusion, the energy transition is a path fraught with social, energy, environmental and economic pitfalls. Reading between the lines of the World Energy Outlook 2021, it appears that an oil and/or gas shock is likely in the coming years (a gas shock might already be existing today). This shock, coupled with exponentially decreasing EROI for oil and gas, and a slow evolution for renewables (themselves lower), represents a structural risk for our societies. At both the national and international levels, it seems prudent and even necessary, even in the absence of climate constraints, to accelerate the energy transition by emphasizing sobriety, while anticipating a more competitive and conflictual world.

Notes

[1] Reuters News & Media, Morgan Stanley cuts Q1 2022 Brent oil forecast on Omicron risks, Commodities, 29 November 2021.

[2] Delannoy, L. et al. (2021), Peak oil and the low-carbon energy transition: A net-energy perspective, Applied Energy, Vol. 304, 15 December 2021.

[3] Delannoy, L. et al. (2021), Assessing Global Long-Term EROI of Gas: A Net-Energy Perspective on the Energy Transition, Energies, Vol. 14 (16), 19 August 2019.

[4] Brockway, P. et al. (2019), Estimation of global final-stage energy-return-on-investment for fossil fuels with comparison to renewable energy sources, Nature Energy, Vol. 4, 11 July 2019.

[5] Jackson, A. & Jackson, T. (2021), Modelling energy transition risk: The impact of declining energy return on investment (EROI), Ecological Economics, Vol. 185, July 2021.

|

ABOUT THE AUTHOR

Louis Delannoy is a PhD fellow in the STEEP research team at INRIA (French National Institute for Research in Digital Science and Technology). He is also attached to the Jean Kuntzmann Laboratory, the MSTII doctorate school of the Grenoble Alpes University and the Petroleum Analysis Centre. His research focuses on global systemic risks, their causes and consequences. More specifically, he examines how crisis transmit to the economy and whether cascading failures can lead to a contagion collapse scenario, using system dynamics modeling and statistical methods. He holds a Master of Science in Energy Management & Sustainability from the Swiss Federal Institute of Technology in Lausanne (EPFL).

|

![[groups_small]](groups_small.gif)