|

Mother Pelican

A Journal of Solidarity and Sustainability

Vol. 14, No. 7, July 2018

Luis T. Gutiérrez, Editor

|

|

|

|

|

|

|

Will EROI be the Primary Determinant of Our Economic Future?

The View of the Natural Scientist versus the Economist

Charles Hall

Originally published in

Joule, Volume 1, Issue 4, 20 December 2017

REPRINTED WITH PERMISSION

|

Two philosophical worldviews as to how the future of energy will play out exist within the confines of economics and science. Each is reflected profusely and erratically in the blogosphere. The first is that of human determinism associated with human cleverness and technological cornucopianism, the second assumes that human determinism is largely underwritten by energy subsidies and will ultimately be constrained by larger forces of nature. These two world views are playing out now in two principal, and as yet unresolved, issues related to energy. The first is whether prices are all that is needed to make decisions about energy, and the second is whether, to decrease impacts of climate change or depletion, we can replace the carbon-intensive fossil fuels that dominate our energy use with something else, such as biomass, photovoltaics, and wind turbines. Presently, most of these decisions are based on economic analyses by corporations and government agencies except as influenced by the legislated terrain. But prices are hugely influenced by subsidies, and the presence or absence of externalities, and reflect far more the present than a possibly very different future.

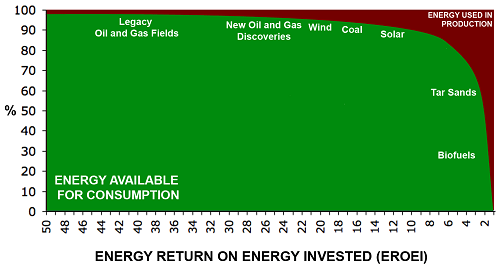

Energy Return on Energy Invested (EROEI)

Energy return on investment (EROI, sometimes EROEI) is a tool (or metric) that avoids some of the problems with financial analysis while generating additional insight into the factors that influence present prices and future availabilities. EROI is simply the energy delivered from a process divided by the energy required to get it. A lower EROI means that society must divert more of its total economic activity to get the energy to run the rest of the economy. EROI integrates the counteracting effects of depletion and technological improvements. An important issue is the energy cliff. Changes in EROI at relatively high values, above say 10:1, have much less impact than changes at lower values. Historically, the view of economists has been that depletion is not an issue for the future of economic production because the higher prices that will result will encourage a reduction in use and the substitution of alternatives, including lower-grade resources. EROI provides a bullet-proof response to the economists' argument that ever lower grades can be used indefinitely. Curiously, it is based on economist David Ricardo's concept that humans use the best resources first. As higher grades are depleted, the energy required increases. At some point, the energy input is as great as the energy output, and the resource is no longer economic in any sense except where some cheaper fuel is used to get more expensive fuel. There are many important oil (and oil substitute) resources that are already at or near this point, including many of our legacy oil wells in the United States and China, oil shale (kerogen), corn-based ethanol, and tar sands1xEnergy Return on Investment: A Unifying Principle for Biology, Economics and Sustainability. Hall, C.A.S.

Crossref | Google ScholarSee all References, 2xEnergetic productivity dynamics of global super-giant oilfields. Masnadi, M.S. and Brandt, A.R. Energy Environ. Sci. 2017;

10: 14931504

Crossref | Google ScholarSee all References. The argument usually thought by economists to resolve this issue, in favor of technology, is that of Barnett and Morse,3xScarcity and Growth: The Economics of Natural Resource Availability. Barnett, H.J. and Morse, C.

Google ScholarSee all References who examined the inflation-corrected cost of a series of raw materials during the mid-20th century. They found that over time, the prices of nearly all decreased or stayed the same even as depletion advanced, implying that depletion was countered by improved technology. These results cemented in the minds of most economists the argument that depletion was not an issue that they had to worry about. A second argument was based on the work of Denison who examined the increase in GDP of the US economy during much of the twentieth century and found that increases in capital and labor could explain only about half of the increase in GDP. Denison attributed the remaining increase (the Solow residual) to increases in technology or pure human ingenuity. The declining energy use per unit of GDP for some highly developed nations is also used to argue for the positive impact of technology. In fact all of these arguments used by economists collapse when examined in the context of energy. Cleveland4xScarcity and growth revisited. Cleveland, C. : 289317

Google ScholarSee all References found that during the time period of Barnett and Morse's analysis, the price of energy declined, and this allowed an increase in the use of energy necessary to compensate for depletion without increasing production costs. Kummel added energy to labor and capital in Denison's analysis and found that not only did the technological residual disappear but that energy was more important than either capital or labor for explaining the increase in GDP. Weidman et al.5xThe material footprint of nations. Wiedmann, T.O., Schandl, H., Lenzen, M., Moranc, D., Suh, S., West, J., and Kanemotoc, K. Proc. Natl. Acad. Sci. USA. 2012;

112: 62716276

Crossref | Scopus (269) | Google ScholarSee all References found that, with the use of appropriate accounting for imports, increases in global economic production continues to be associated with a commensurate increase in the use of materials (including energy), i.e., there has been little increase in the efficiency by which all nations collectively turn materials from the Earth into wealth.

History of EROIThe concept of EROI has been around as net energy (energy delivered minus energy cost to get that energy) for at least 100 years, associated especially with sociologists Leslie White and Frederick Cottrell and ecologist Howard Odum in the middle of the last century. The term EROI was derived in my own studies of fish migration and first used explicitly for fossil fuels by myself and colleagues in a series of papers and books in the late 1970s and 1980s (e.g., Cleveland et al.6xEnergy and the United States economy: a biophysical perspective. Cleveland, C.J., Costanza, R., Hall, C.A.S., and Kaufmann, R. Science. 1984;

225: 890897

Crossref | PubMed | Scopus (403) | Google ScholarSee all References; reviewed in Hall1xEnergy Return on Investment: A Unifying Principle for Biology, Economics and Sustainability. Hall, C.A.S.

Crossref | Google ScholarSee all References). There has been a resurgence of interest in the last decade, including studies under the aegis of Energy Payback Time. These studies show that the EROI of most major fossil fuels were traditionally high (>20:1) but are declining, most new renewable fuels have a relatively low EROI except perhaps for photovoltaics (PV) and wind (see below), compensating for intermittency is important and largely unknown, and that while EROI is not a precision science, increasingly we find that when similar boundaries and assumptions are used the values tend to converge. Given that here has been essentially no government funding for this critical research area, the applications are impressively diverse and results consistent.

Economic Implications of Changing EROIIt is clear that our increasing wealth in the last several centuries is closely associated with the use of more and higher EROI fossil fuels. Subsidizing labor with fossil fuels has given each worker much higher productivity. Long-term historical analysis indicates that for the period 1300 to 1750 in England on the order of one-third to one-half of all economic activity was required to get the energy required (in this case food, firewood, fodder) to run all economic activity, implying an EROI of 23:1.7xComparing world economic and net energy metrics, part 3: macroeconomic historical and future perspectives. King, C.W. Energies. 2015;

8: 12348

Google ScholarSee all References With the advent of fossil fuels, the EROI increased to 20:1 or more and only 5%10% of all economic activity was necessary to get fuel. Society became much richer and was transformed from stability to one in which year to year economic growth occurred and was considered normal (until recently).

Current Issues and Criticisms Pertaining to EROIThere have been a number of debates and criticisms of the concepts and the specifics of EROI in both the reviewed literature and the general blogosphere. These include whether corn-based ethanol generates a net energy profit, whether PV generates a sufficiently high EROI to be financially feasible, and more general criticisms examined in Hall.1xEnergy Return on Investment: A Unifying Principle for Biology, Economics and Sustainability. Hall, C.A.S.

Crossref | Google ScholarSee all References The first important controversy pertaining to EROI was the issue of whether corn-based ethanol was an energy source or sink. Several authors, including Kim and Dale, found that corn-based ethanol would return at least 1.7 J of energy for every joule invested in its production, i.e., in making the required fertilizer, operating tractors for planting, cultivating, and harvesting, while other analysts (e.g., Pimentel and Patzek) found that the return was less than 1:1. Hall, Dale, and Pimentel examined these differing studies and found that the main reason for the differences was whether credit was given to the residual from distilling the alcohol, which could be used for animal feeds, and some relatively small differences in the energy costs of, e.g., fertilizers. Presently, the main controversy pertains to differences in estimates of EROI for PV (e.g., Prieto and Hall8xSpain's Photovoltaic Revolution: The Energy Return on Investment. Prieto, P.A. and Hall, C.A.S.

Crossref | Google ScholarSee all References estimate an EROI of 3:1 or less for PV systems in Spain, whereas Raugei et al.9xThe energy return on energy investment (EROI) of photovoltaics: methodology and comparisons with fossil fuel life cycles. Raugei, M., Fullana-i-Palmer, P., and Fthenakis, V. Energy Policy. 2012;

45: 576582

Crossref | Scopus (89) | Google ScholarSee all References give estimates of at least 10:1). The main reason for this large difference is whether or not the output of the PVs, which is high-quality electricity, is or is not weighted for the fossil fuel avoided. A second reason is the boundaries used: Prieto and Hall attempted to account for all of the energy used to operationalize actual projects. If these issues are accounted for, the numbers tend to be much closer. The energy cost of dealing with intermittency remains unresolved. The EROI issue appears critical in determining the degree possible, and the economic consequences, of replacing fossil fuels with renewables to attempt to protect the climate.

Explicit Critiques of EROI by EconomistsIn a recent meeting of scientists and economists in London, economists raised eight points as to why it was not necessary to consider EROI in determining future energy availability or policy. I list and answer each: - 1. Energy's cost share is only 5%10% of GDP, so the contribution of energy productivity to growth is much smaller than the contributions of labor productivity, capital productivity, and innovation.

Response: I argue that instead the low-cost share of energy is the reason for its importance: energy has been cheap relative to its importance in economic production, which Kummel has shown is greater than either capital or labor. One can also see the importance of energy in the analysis of Hamilton10xCauses and consequences of the oil shock of 2007-2008. Hamilton, J. Brooking Papers on Economic Activity. 2009;

Spring: 215283

Crossref | Google ScholarSee all References who found that whenever energy costs approached 10% of GDP, a recession follows.

- 2. Energy is only one input to the cost of producing energy. All the other inputs matter as well. If energy input is high (so EROI >1:1 but very low), but other input costs are minimal, then it is not a problem. As long as other input costs are very low, you can do as much of it as you like.

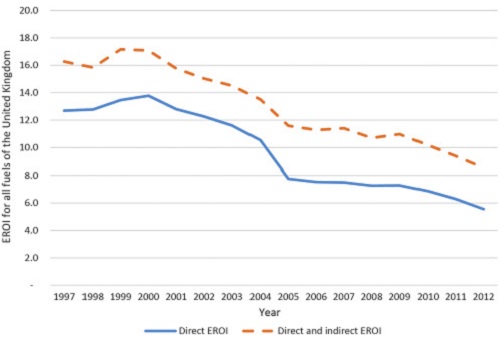

Response: The price and efficacy of capital and labor are also determined in part by the efficiency of the energy economy. If EROI is very low, then a larger portion of all economic activity, including capital and labor, must be devoted to the energy sector, pushing up the costs of everything. While it is true that a decline in EROI probably makes relatively little impact when EROI is above 10 or 20:1 (i.e., far from the energy cliff), our main fuels have been approaching or going below that level recently (reviewed in Hall1xEnergy Return on Investment: A Unifying Principle for Biology, Economics and Sustainability. Hall, C.A.S.

Crossref | Google ScholarSee all References; Figure 1Figure 1).  Figure 1

Figure 1. EROI of all fossil fuels for the United Kingdom including only the energy used on site (dotted red line) and also including the indirect energy (solid blue line) used off site (e.g., for manufacturing platforms).11

|

xDeveloping an input-output based method to estimate a national-level energy return on investment (EROI). Brand-Correa, L.I., Brockway, P.E., Copeland, C.L., Foxon, T.J., Owen, A., and Taylor, P.G. Energies. 2017;

10: 534

Crossref | Scopus (5) | Google ScholarSee all References

- 3.

What really matters is not EROI, but cost.

Response: That may be true, but King and Hall found that for US oil and gas, costs and EROI are statistically inverse. If and as EROI continues to decline in the future, energy costs will inevitably increase. Lambert et al.12xEnergy, EROI and quality of life. Lambert, J., Hall, C.A.S., Balogh, S., Gupta, A., and Arnold, M. Energy Policy. 2014;

64: 153167

Crossref | Scopus (74) | Google ScholarSee all References develop arguments and data as to why relatively high EROIs are important for providing the amenities we take for granted in modern societies.

- 4. Oil prices are low at the moment, so that suggests that either EROI is not falling to a low level, or that if it is falling to a low level, then this is not affecting cost.

Response: Oil prices, corrected for inflation, are at a historical moderate price. Part of the reason may be that oil's recent high and still moderate price may have dampened economic growth in the OECD countries, consistent with the model of Murphy and Hall.1xEnergy Return on Investment: A Unifying Principle for Biology, Economics and Sustainability. Hall, C.A.S.

Crossref | Google ScholarSee all References Supply and demand also influence prices, and supply now is relatively high relative to demand, which has been flat. Most of the small increase in global oil production is from fracked technology in the US, where prices are low in part because oil companies are not making profits.

- 5. If falling EROI has not made much difference to cost so far, that is because there is not much difference between 100:1 and 10:1. This would not be expected to make much difference to cost or to produce much difference in investment.

- 6. If EROI declines to a low enough level to make a difference to costs, then we would expect that at that point the price signal will lead to higher investment, technological progress, and EROI going back up.

Response: Greater investments in money usually means greater investment in energy. There is little or no evidence that investments lead to higher EROI for conventional fuels, in fact EROI of all main fossil fuels we are aware of are declining despite considerable investments in technology (see review in Hall1xEnergy Return on Investment: A Unifying Principle for Biology, Economics and Sustainability. Hall, C.A.S.

Crossref | Google ScholarSee all References).

- 7. There is no problem of scarcity of fossil fuels. Evidence is that there are huge amounts of unconventional resources, and we are barely scratching the surface. There is much more than we can use if we are going to limit climate change in line with the 2°C target.

Response: there is no question that there are huge resources left of low-grade fossil fuel. But this is where EROI becomes critical: essentially all large-scale alternatives are lower EROI. For example, tar sands have an EROI of about 4:1 and Colorado oil shales close to 1:1. So far, the many efforts to exploit these have failed or are economically marginal.

- 8. Experience so far is that the price signal has a very strong effect in opening up new technologies, new reserves, and substitution; so even if prices do rise in future, that is not necessarily a bad thing.

Response: Exactly: in a Ricardian way humans use higher-quality, high-EROI resources first. This we have done with fossil fuels for decades and centuries. The EROI of all conventional energy resources (except US coal) have been declining as depletion has been more important than technical improvements. We are already depleting the best fracked oil resources (e.g., Montrose County, North Dakota) even as the production and EROI of our traditional elephants, the large fields that still supply the majority of our oil but no longer find, decline (Hallock et al.13xForecasting the limits to the availability and diversity of global conventional oil supply: validation. Hallock, J.L. Jr., Wu, W., Hall, C.A.S., and Jefferson, M. Energy. 2014;

64: 130153

Crossref | Scopus (28) | Google ScholarSee all References; Masnadi and Brandt2xEnergetic productivity dynamics of global super-giant oilfields. Masnadi, M.S. and Brandt, A.R. Energy Environ. Sci. 2017;

10: 14931504

Crossref | Google ScholarSee all References).

So as a very general response to the economist's arguments, I would say that what they are saying is quite in line with standard economic theory and economic thinking, but that a careful examination of the data using a biophysical approach shows that the economic assumptions are not necessarily reflected in actual behavior of economic systems. Over the longer term, EROI is likely to continue to decline, which will have increasing impact. In conclusion, my opinion is that economic dogma is very comforting, and partially consistent with some data, but that a careful examination of actual data shows that nature does not necessarily follow economic theories. Meanwhile, analyses that we have by people very familiar with the oil industry suggest that Hubbert's peak oil theory is alive and well, although perhaps delayed by a decade or two (e.g., Mohr et al.14xProjection of world fossil fuels by country. Mohr, S.H., Wang, J., Ellem, G., Ward, J., and Giurco, D. Fuel. 2015;

1: 120135

Crossref | Scopus (91) | Google ScholarSee all References). A decline in EROI will exacerbate whatever economic problems ensue.

References

1 Hall, C.A.S. Energy Return on Investment: A Unifying Principle for Biology, Economics and Sustainability. Springer-Nature,

; 20172 Masnadi, M.S. and Brandt, A.R. Energetic productivity dynamics of global super-giant oilfields. Energy Environ. Sci. 2017;

10: 149315043 Barnett, H.J. and Morse, C. Scarcity and Growth: The Economics of Natural Resource Availability. Johns Hopkins University Press,

; 19634 Cleveland, C. Scarcity and growth revisited. in: R. Costanza

(Ed.)

Ecological Economics: The Science and Management of Sustainability. Columbia University Press,

; 1991: 2893175 Wiedmann, T.O., Schandl, H., Lenzen, M., Moranc, D., Suh, S., West, J., and Kanemotoc, K. The material footprint of nations. Proc. Natl. Acad. Sci. USA. 2012;

112: 627162766 Cleveland, C.J., Costanza, R., Hall, C.A.S., and Kaufmann, R. Energy and the United States economy: a biophysical perspective. Science. 1984;

225: 8908977 King, C.W. Comparing world economic and net energy metrics, part 3: macroeconomic historical and future perspectives. Energies. 2015;

8 : 123488Prieto, P.A. and Hall, C.A.S. Spain's Photovoltaic Revolution: The Energy Return on Investment. Springer-Nature,

; 20139 Raugei, M., Fullana-i-Palmer, P., and Fthenakis, V. The energy return on energy investment (EROI) of photovoltaics: methodology and comparisons with fossil fuel life cycles. Energy Policy. 2012;

45: 57658210 Hamilton, J. Causes and consequences of the oil shock of 2007-2008. Brooking Papers on Economic Activity. 2009;

Spring: 21528311 Brand-Correa, L.I., Brockway, P.E., Copeland, C.L., Foxon, T.J., Owen, A., and Taylor, P.G. Developing an input-output based method to estimate a national-level energy return on investment (EROI). Energies. 2017;

10: 53412 Lambert, J., Hall, C.A.S., Balogh, S., Gupta, A., and Arnold, M. Energy, EROI and quality of life. Energy Policy. 2014;

64: 15316713 Hallock, J.L. Jr., Wu, W., Hall, C.A.S., and Jefferson, M. Forecasting the limits to the availability and diversity of global conventional oil supply: validation. Energy. 2014;

64: 13015314 Mohr, S.H., Wang, J., Ellem, G., Ward, J., and Giurco, D. Projection of world fossil fuels by country. Fuel. 2015;

1: 120135Published online: October 12, 2017 ~ © 2017 Elsevier Inc.

|

ABOUT THE AUTHOR

Charles A.S. Hall is a Systems Ecologist who received his PhD under Howard T. Odum at the University of North Carolina at Chapel Hill in 1970. He was professor over the past 45 years at Cornell University, the University of Montana, and the College of Environmental Science and Forestry of the State University of New York. He is now retired (but very active as Professor Emeritus) in Western Montana. Dr. Hall is the author or editor of 14 books and 300 scholarly articles and has been awarded the distinguished Hubbert-Simmons Prize for Energy Education and the Lifetime Achievement Award from the International Society of BioPhysical Economics. He is best known for his development of the concept of EROI, or energy return on investment, which is an examination of how organisms, including humans, invest energy into obtaining additional energy to improve biotic or social fitness, and also a new field, BioPhysical Economics, as a supplement or alternative to conventional economics. He has applied systems and EROI thinking to a broad series of biological, resource, and economic issues in more than 30 countries. His most recent books are Energy and the Wealth of Nations: An Introduction to BioPhysical Economics (with Kent Klitgaard), America's Most Sustainable Cities and Regions (with John Day), and Energy Return on Investment. A unifying Principle for Biology, Economics and Sustainability, all available from Springer. He is coeditor with Ugo Bardi and Gaël Giraud of the journal BioPhysical Economics and Resource Quality.

|

|Back to Title|

LINK TO THE CURRENT ISSUE

LINK TO THE HOME PAGE

|

|

|

|

"The future is greater than all the past."

Pierre Teilhard de Chardin (1881-1955)

|

|

Page 9

|

|

FREE SUBSCRIPTION

|

![[groups_small]](groups_small.gif)

|

Subscribe to the

Mother Pelican Journal

via the Solidarity-Sustainability Group

Enter your email address:

|

|

|

|

{kind=link}