China took the world by surprise with its sustained, rapid, coal-intensive growth of the early twenty first century. It contributed a majority of the growth in global coal use and greenhouse gas emissions from 2000 to 2011. This caused considerable pessimism about humanitys capacity to hold human-induced increases in temperature within reasonable limits, and introduced new tension into international discussions of climate change mitigation. These developments in China pushed global emissions above the highest of the many scenarios for the future that had been developed by the Intergovernmental Panel on Climate Change (IPCC).

And then China took the world by surprise again. The pattern of Chinese economic growth changed, towards less energy-intensive activity and less emissions-intensive energy. The effects of the structural change showed up in the statistics from 2012, and more decisively in each year after that. The changes in China have again transformed expectations of what is possible in global climate change mitigation, this time in a positive direction.

The same pattern of urban and industrial growth that exacerbated global warming in the early twenty first century also imposed huge damage on local natural systems. The impact that was most immediately harmful to people and most provocative to social and political stability was a dramatic increase in air pollution in and near Chinas large cities. By 2013, these domestic

environmental issues were strongly reinforcing other pressures for changes in economic policy and structure.

Chinas new model of development improves the chances of the international community meeting the 2 degrees climate target. It is starting to slow the deterioration in local environmental amenity in Chinas cities. And as China shifts its own production towards sustainable patterns, it demonstrates to other developing countries that continued economic growth can be consistent with reduced pressure on the environment. The huge scale of Chinese deployment of low-emissions technologies is reducing the cost of environmentally sustainable development for itself and for other countries.

This evenings lecture describes the old model of growth that reached its apogee in the first eleven years of this century, and the new patterns that are replacing it. It focusses mainly on climate change with its global context, but touches upon local environmental issues.

Why China matters to climate change and climate change matters to China

The way that the international community manages human-induced climate change will shape Chinas future. Chinas own policy will have large influence on how much damage is done to China and the rest of the world by climate change. Strong and effective mitigation in China is a necessary condition for achieving the United Nations goal to hold human-induced increases in temperature to two degrees. It is a necessary but not a sufficient condition, as all other

substantial countries will also have to make large contributions. Chinese policy and diplomacy will influence the actions of other countries.

The good news is that there is close compatibility between policies that China now favours for its own development, and the policies that are necessary for China to do its fair share in an effective global mitigation effort.

Chinese atmospheric science is of high quality. For more than two decades Chinese scientists have been alerting leaders to the risks for China from destabilization of flows in the great rivers, drying of the North China Plain and increases in sea levels affecting human settlements in the coastal commercial and industrial cities. Chinas leaders are aware that China shares

with Australia and all other countries in the Asia Pacific region an interest in avoiding the international political instability that would emerge from the impact of unmitigated climate change in Southeast and South Asia (Dupont and Pearman 2006).

Chinese leaders have heeded scientific advice and attached importance to Chinas

participation in work to combat climate change since the beginning of the international effort more than two decades ago. However, it is only relatively recently that Chinese leaders have absorbed into policy formation the increasingly important reality that Chinese domestic and

diplomatic actions are major determinants of the success of global climate change mitigation.

A new model of economic development has been emerging in China over the past half dozen years, and was influential in the 12th Five-Year Plan 2011-15 (Garnaut et al 2013; Song et al 2014). Over the past two years it has been elaborated by President Xi Jinping and Premier Li Keqiang and endorsed by the 18th Conference of the Chinese Communist Party in 2012, the 3rdPlenary Meeting of the 18th Central Committee in 2013, the March 2014 National Peoples Congress, and subsequent meetings of the State Council. Structural change that is necessary to sustain good economic performance as defined within the new model of economic growth will provide sound foundations for major reductions in the trajectory and soon the absolute level of Chinese greenhouse gas emissions.

China and global emissions

Despite its large population, China contributed relatively little to the increase in atmospheric concentrations of greenhouse gases up to the time the United Nations meeting in Rio de Janeiro made human-induced climate change a major focus of international cooperation. In 1992, the average Chinese emissions of greenhouse gases were less than for the world as a whole and the average historical contribution much less. I recall discussing these issues with

the then Chinese Minister for Environment around the time of the Rio Summit. China recognizes that there is a substantial global problem, he said, and recognizes that it must be part of the solution. But the solution of which it is part has to be a fair solution. And it wouldnt be fair if Chinese emissions per person were restricted to less than the average of the world as a whole.

That seemed at the time to be a reasonable response. It still seems reasonable. But the success of Chinese development over the past two decades changes fundamentally the implications of the principle articulated by the Minister.

The rapid economic expansion in China in the 1990s was accompanied by big reductions in the energy intensity and emissions intensity of production, as an increasing role for prices in resource allocation caused energy to be used more efficiently. Large reductions in emissions intensity in China and for different reasons in what had once been the Soviet Union and the centrally planned economies of Eastern Europe encouraged complacency about long term trends in global emissions.

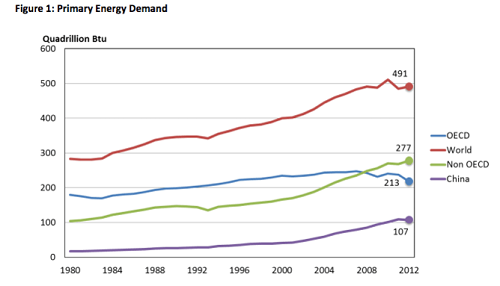

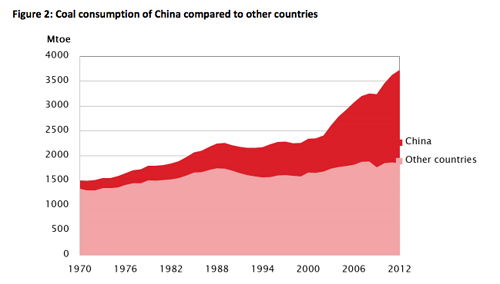

The falls in emissions intensity in China in the 1990s turned out to be once-for-all changes. Chinese greenhouse gas emissions grew strongly in the first eleven years of the new century for three reasons: economic growth was stronger than ever (an average of about 10 percent per annum); the improvement in energy efficiency stopped; and the emissions intensity of energy use remained high as coal maintained and even enhanced its position in energy supply. China became the source of more than half the increase in global greenhouse gas emissions, even more for a while after the Great Crash of 2008 reinforced the role of state-connected investment in the Chinese economy and slowed growth in the old developed countries. China accounted for 21 percent of the increase in world primary energy demand from 1990-2000, and for 52 percent from 2000 to 2011. China accounted for 86 percent of the total world increase in consumption of coal from 1990 to 2011 (International Energy Agency 2013). Chinas

coal combustion in electricity generation increased at a compound rate of over 11 percent per annum from 2001 to in 2011. Extraordinary expansion in steel and cement production contributed to total coal use growing even more rapidly in the first decade of the century, at a compound rate of nearly 13 percent per annum (International Energy Agency, China Data Base, Figures 1 and 2).

Source: BP Statistical Review of World Energy, International Energy Agency

|

Source: BP Statistical Review of World Energy, International Energy Agency

|

The acceleration of growth in global greenhouse gas emissions from the beginning of the new century to 2011 was overwhelmingly the result of acceleration of coal use. Increase in global emissions from coal combustion was overwhelmingly from increased coal use in China (International Energy Agency 2013; Citibank 2013).

The increased Chinese coal use and emissions was one consequence of a brilliantly successful economic growth strategy that greatly increased the living standards of the vast majority of Chinese people and underpinned Chinas emergence as a great economic power. The successful strategy was built on an unprecedentedly high investment share of expenditure, an unprecedentedly high profit (and low wages) share of income, exceptionally low proportions of expenditure on consumption and on services, and great pressure on domestic and global environmental amenity and stability (Garnaut et al 2014).

After the first half dozen years of the new century, the Chinese government and people began to reassess the old growth model. While it was widely recognized that the old model had generated large benefits for the Chinese people, its success had created the need for change.

Developments in the Chinese labour market were in any case generating pressures for change. The deceleration of growth and then decline in the work-age population interacted with continued strong growth in demand for labour to generate shortages of in major coastal cities from about 2005 and then more broadly through the economy (Cai 2014). Wages have grown more rapidly than the economy since the Great Crash of 2008. This was bound eventually to put downward pressure on the investment share of expenditure.

Meanwhile, higher incomes for most Chinese brought increased sensitivity about inequality in incomes and access to services. They also made room for increased concern about environmental amenity. The damaging effects of carbon pollution on health and longevity became more important in public discussion, reinforced by scientific evidence that greater environmental degradation associated with more intense use of coal and other fossil fuels contributed substantially to lower life expectancy in parts of China that used them most intensively (Chen et al 2013; Sheehan et al 2014).

These changes in priorities encouraged new domestic policies to increase services available to low-income Chinese everywhere and especially in the countryside. New regulations were developed to protect the domestic environment.

China at the United Nations conferences at Copenhagen in 2009 and Cancun in 2010 made strong commitments to change the relationship between economic growth and greenhouse gas emissions. It advised the United Nations Framework Convention on Climate Change that it would reduce the emissions intensity of economic activity by 40-45 percent between 2005 and 2020. The new model of economic growth made the achievement of this objective possible.

Chinas emissions in the new Chinese model of economic growth

Changes in the new growth model in China

The new model of economic growth involves some changes that flow inevitably from Chinas demographic and economic circumstances and some that result from new policy choices. Altogether the new model envisages decline in the investment share of expenditure and increase in the consumption share, especially consumption of services. It is built on expectations of a decline in the labour force and slower growth in the capital stock, leading to overall growth being several percentage points lower than in the first decade of the century. It

envisages market-oriented economic reform to increase the productivity with which resources are used, with the potential to offset some of the fall in the growth rate. The focus on increased productivity includes efforts to reduce the amount of energy consumed in producing each unit of economic output. The new model of economic growth contains strong commitments to expansion of public services and social security provision, especially in rural areas. It embodies a wide range of interventions to reduce domestic and international environmental damage from continued economic growth.

Many of the structural changes embodied in the new model of economic growth have large and favourable implications for greenhouse gas emissions.

A fall in the investment share of expenditure can be expected to reduce emissions. The government has not quantified its ambition for reduction in the investment share. Simple economic arithmetic tells us that this fall could be large: a step down from 10 percent per annum growth to 7.5 percent would reduce by one quarter the absolute level of investment if capital-output ratios remained constant. The aim of the Chinese Government is for the fall in

investment to be replaced by an increase in consumption especially of services, with much lower use of metals and energy and much lower emissions of greenhouse gases per unit of economic value.

The 12th Five-Year Plan embodies an expectation of a fall in energy use per unit of output of 16 percent over 5 years. It anticipates a 17 percent reduction in emissions intensity.

The policies being applied to break the old nexus between economic output and greenhouse emissions are extensive, and have the potential to reduce Chinese emissions by more than is required to meet the target advised to the United Nations.

The Chinese economy is a big ship, and takes time to turn. Elements of the new model of economic growth were being discussed and in some cases implemented for some years before the 12th Five-Year Plan. The new goals and approaches were embedded more systematically in the Plan for 2011-15. Policies have been elaborated and applied with increased strength in each year of the Plan.

The fall in the trend rate of growth in economic output from around 10 percent in the decade to 2011 to 7-8 percent since then itself reduced the rate of increase in emissions. So far there has not been any significant fall in the investment share of expenditure despite the lower rate

of growth.

After a slow start in 2011, the fall in energy intensity is now proceeding rapidly. In 2012, an improvement of 4 percent in energy efficiency was, with the United States and Russia, at the forefront of global achievement (International Energy Agency 2013). There was a similar reduction in 2013. The eventual fall in the investment share of GDP can be expected to extend the decline in energy intensity of output. Other policy interventions have caused the rate of

decline in emissions intensity to exceed that for energy intensity.

Emissions reductions in electricity

There have already been remarkable reductions in emissions intensity in electricity generation since 2011. This has been achieved partly through reducing the electricity used in incremental economic production and especially through the substitution of alternative sources of electricity for coal in supplying the increase in electricity generation.

In China, as in many countries, electricity generation accounts for more emissions than any other activity. Moreover, decarbonisation of electricity generation can provide a path to radical reduction of emissions in transport (electric trains and automobiles) and some industrial processes.

(*) Calculated as a residual. Calculated as a residual from other hypotheticals. Tables 1, 1a, 2 and 2a Sources: The following People's Republic of China official sources were consulted: Twelfth Five-Year Plan; Chinese Electricity Development Twelfth Five-Year Plan; Chinese Energy Conservation and Emission Reduction Twelfth Five-Year Plan; Chinese Natural Gas Development Twelfth Five-Year Plan; National Energy Work Conference 2014; Chinese National Energy Administration Annual reports; China Coal Industry Association Annual reports; 2014 announcements of State Council and National Development and Reform Commission.

|

(*) Calculated as a residual. Calculated as a residual from other hypotheticals. Tables 1, 1a, 2 and 2a Sources: The following People's Republic of China official sources were consulted: Twelfth Five-Year Plan; Chinese Electricity Development Twelfth Five-Year Plan; Chinese Energy Conservation and Emission Reduction Twelfth Five-Year Plan; Chinese Natural Gas Development Twelfth Five-Year Plan; National Energy Work Conference 2014; Chinese National Energy Administration Annual reports; China Coal Industry Association Annual reports; 2014 announcements of State Council and National Development and Reform Commission.

|

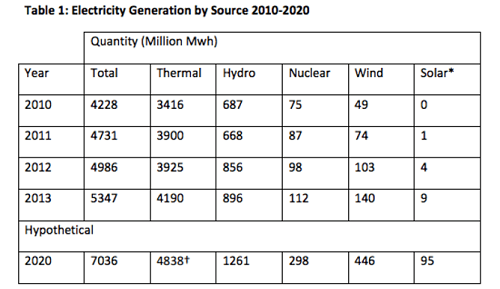

Table 1 sets out recent developments in the sources of energy for electricity generation in China, and suggests a possible path to 2020 on moderate assumptions about the rate of expansion of supply of low-emissions energy. It treats thermal energy as one broad category. Table 2 provides insights into sources of thermal energy in the recent past, and looks forward to 2020 on moderate assumptions about growth in low emissions forms of thermal energy.

Electricity demand increased substantially more rapidly than economic output in the decade before 2011, but less rapidly after that. A combination of lower GDP growth and accelerated reduction in the emissions intensity of production after 2011 sharply reduced energy demand growth.

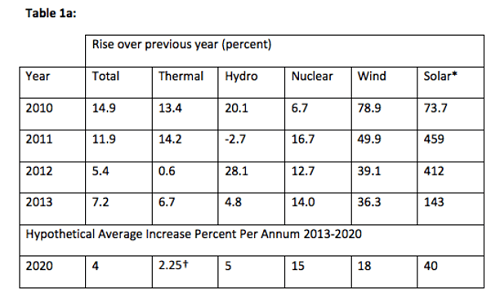

Thermal power in general and coal in particular held or expanded their shares of power generation in the decade to 2011. As a result, growth of over 11 percent per annum in demand for thermal coal exceeded the rate of growth of GDP. The story has been different since then, with low emissions energy accounting for the majority of the slower increase in electricity output. The hydroelectric component of low emissions energy has been dominant, fluctuating with seasonal conditions around a strong upward trend. Once renewables capacity has been

installed and connected to the grid it tends to be utilized ahead of thermal capacity, as its operating costs are low. The fluctuations in availability of hydroelectric capacity are therefore transmitted inversely into fluctuations in rates of growth of thermal including coal-based generation. After a decade in which coal used in power generation increased by over 11 percent per annum, the volume of coal used in power generation in 2013 was only 4-5 percent above that two years before. Nuclear power output has been growing solidly, and wind more

rapidly to levels that now exceed nuclear. Solar is growing most rapidly of all from a zero base a few years ago, and is becoming a significant element in the electricity mix.

In Table 1, total demand for thermal electricity in 2020 is derived from estimates of growth in GDP (assumed at 7 percent per annum from 2013 to 2020) and reductions in the ratio of electricity to total output (assumed at 3 percent per annum). The hypothetical numbers on power demand growth in Table 1 assume a slowing of the rate of reduction in the ratio of electricity to total output from levels attained in 2012 and 2013. This goes beyond current official projections in reductions of growth in electricity demand, but is consistent with the likely interaction of tendencies in Chinese energy policy, the prospective fall in the investment share of GDP and technological potential as revealed in the recent experience of developed countries. Confidence in the continued reduction of the ratio of electricity use to GDP can be

drawn from the general tendency for electricity demand to fall absolutely in developed countries since 2008, even in countries experiencing reasonably strong economic growth (Garnaut 2014). On the other hand, the electrification of transport and some industrial processes may have the opposite effect. The main effects of transport and industrial electrification will come after 2020; to the extent that change before 2020 is more rapid than expected, it will slow the rate of decline in intensity of fossil fuel use in electricity generation

and accelerate it in transport and industrial processes.

The hypothetical future numbers in Table 1 also adopt moderate assessments for the growth in wind, nuclear and solar power in 2020. All are well below recent growth rates, and within official expectations for the sources of energy when discussed in isolation.

An increasing proportion of electricity coming from intermittent (wind and solar) and non-variable (nuclear) sources generates challenges for stability of the grid. For many regions, the presence of large hydro electric capacity which can be varied over short periods facilitates balancing the grid and can continue to do so. Over recent years, even larger investments have been made in upgrading the electricity grid than in generation, much of it to facilitate absorption of intermittent and non-variable power. These include large pumped hydro storage

facilities (a total of 30Gw capacity to be installed by 2015) adjacent to many of Chinas large cities. Improvements in the grid and expanded storage facilities have facilitated more complete utilization of low-emissions capacity (Peoples Republic of China 2011).

(*) Calculated as a residual. Calculation on assumption that the amount of coal per Mwh continues to fall by an average of 1 percent per annum as a result of replacement of environmentally inefficient generators by supercritical capacity. See Mai and Feng 2013 which suggests 1.5 percent per annum and the 12th Five-Year Plan which suggests 0.6 percent per annum. Based on assumption that state will achieve an objective of 7.5% of power from gas by 2020. Tables 1, 1a, 2 and 2a Sources: The following People's Republic of China official sources were consulted: Twelfth Five-Year Plan; Chinese Electricity Development Twelfth Five-Year Plan; Chinese Energy Conservation and Emission Reduction Twelfth Five-Year Plan; Chinese Natural Gas Development Twelfth Five-Year Plan; National Energy Work Conference 2014; Chinese National Energy Administration Annual reports; China Coal Industry Association Annual reports; 2014 announcements of State Council and National Development and Reform Commission.

|

(*) Calculated as a residual. Calculation on assumption that the amount of coal per Mwh continues to fall by an average of 1 percent per annum as a result of replacement of environmentally inefficient generators by supercritical capacity. See Mai and Feng 2013 which suggests 1.5 percent per annum and the 12th Five-Year Plan which suggests 0.6 percent per annum. Based on assumption that state will achieve an objective of 7.5% of power from gas by 2020. Tables 1, 1a, 2 and 2a Sources: The following People's Republic of China official sources were consulted: Twelfth Five-Year Plan; Chinese Electricity Development Twelfth Five-Year Plan; Chinese Energy Conservation and Emission Reduction Twelfth Five-Year Plan; Chinese Natural Gas Development Twelfth Five-Year Plan; National Energy Work Conference 2014; Chinese National Energy Administration Annual reports; China Coal Industry Association Annual reports; 2014 announcements of State Council and National Development and Reform Commission.

|

Table 2 looks at the sources of thermal electricity. Coal dominates thermal electricity output. Low emissions gas and zero emissions biomass and cogeneration are increasing rapidly from low bases. The hypothetical growth for biomass and cogeneration are well below recent experience and are conservative. The gas numbers are derived from Chinese official objectives. Their realization depends on rapid expansion of domestic and international supplies. New

pipelines from Russia and Central Asia and terminals to receive and pipelines to distribute LNG from Australia, Papua New Guinea, Southeast Asia, the Middle East and eventually North America are supporting rapid growth in imports. Immense investment in conventional and unconventional gas exploration is showing mixed outcomes in these early days, with both early discoveries and disappointments.

The estimates of thermal power demand for 2020, calculated as a residual, and the low emissions contributions to meeting that demand, leave supply of coal-based power as a second residual. The ratio of coal use to coal-based electricity generation is assumed to fall by 1 percent per annum, reflecting the continued effect of the replacement of small, environmentally and economically inefficient plants by large, efficient plants (Mai and Feng

2013). The projections on cautious assumptions suggest a small decline in thermal coal combustion between 2013 and 20200.1 percent per annum. After the growth of over 11 percent per annum in coal use in power generation in the first eleven years of the century, this is a turnaround of historic dimension and global importance.

The increase in gas use would generate its own increase in greenhouse gas emissions. Taking coal and gas combustion together, overall emissions from electricity generation are projected to increase only slightly from 2013 to 2020, and to decline slightly from 2015 to 2020.

Chinas success in implementing the new model of economic growth is not assured. The Chinese government faces pressures from special interests to desist from changes. This is to be expected: it is never an easy matter anywhere to diminish private benefits that have been taken for granted for a long time. Large structural change is associated with uncertainty, and implementation of the new strategy may cause short-term problems that introduce pressures to retreat from new directions. But while the new model of economic growth faces many challenges, the problems for Chinese prosperity and political and economic stability from pressing ahead will be much smaller than the problems that confront China if the new policies fail.

So long as China succeeds with the new model of economic growth, the projections of coal use in Tables 2 and 2a and the absolute levels of emissions that are implied by it are likely to be towards the high end of the range of possible outcomes.

Some recent official statements envisage rates of nuclear, wind and solar expansion that are higher than suggested in Tables 1 and 1a, and rates of increase in gas power generation could rise to over 8 percent of the total. An important statement from the National Development and Reform Commission, Chinas energy and climate change policy and planning agency, in May 17 2014 upgraded expectations on wind and solar capacity. The 78 Gw of wind power installed at the end of 2013 is now expected almost to double in four years to 150Gw by 2017.

The 20 Gw of solar installed by the end of 2013 is expected to increase to 70Gw in 2017. The increase in Chinese wind capacity over these few years will equal almost double Australias current generation capacity of all kinds. The increase in Chinese solar power capacity will exceed by a wide margin Australias total electricity generation capacity of all kinds.

Emissions reductions in transport and industrial processes

I have not yet completed similar work on the prospects for reducing emissions outside the electricity sector. Others have suggested that the new model of growth is as favourable to containing emissions in the rest of the economy as it is in electricity (Citigroup, 2013, Jiang, 2014). That is plausible. The high emissions intensity of production in China is as exceptional in industry as in electricity generation. This follows partly from the structure of production: China now accounts for over half of global production of steel and cement. Coal use in steel and other metals processing, cement and other industries expanded more rapidly than in electricity generation from 2001 to 2011.

Reduction in the investment share of expenditure will reduce metals intensity, the rising and eventually extreme levels of which contributed strongly to high emissions growth in the first decade of the century. The elevation of environmental objectives leads to downward pressures on transport emissions, reinforces tendencies for deceleration of growth in metals production and encourages investment in biological carbon sinks.

Transport emissions have been growing rapidly but are likely to respond strongly to new incentives and opportunities to reduce emissions intensity.

The huge investment in intercity fast trains and urban commuter rail over the past half dozen years as well as the tendency towards high density of urban settlement makes Chinese transport systems more like the environmentally frugal European and other East Asian patterns than the extravagant North American and Australian models. Truck and passenger motor vehicle traffic are growing rapidly but now have been exposed to regulatory controls on emissions in line with developed countries. This is occurring at a relatively early stage of development, before the automobile fleet has reached anything like its mature size.

China is seeking to build a leading position in deployment and production of the electric automobile. The Government has announced an objective of having 5 million electric vehicles on the roads by 2020. The provision of producer and consumer subsidies make it likely that this target will be met. This will place use of electric vehicles in China well ahead of the developed countries. Chinese electric vehicle production will benefit in advance of other countries from the cost reductions which come with large scale. This will contribute to acceleration of the use of electric vehicles in China and in other countries.

Greater energy efficiency in electric vehicles assists in reduction of emissions from the beginning, even with high carbon intensity of electricity production. The contribution of electric vehicles to reducing emissions will be extended with gradual decarbonisation of electricity supply along the lines projected in Tables 1 and 2.

There will be gradual normalization of Chinas unusually prominent position in emissions-intensive industrial production over the next decade. The change in the structure of the economy will gradually move steel and cement production and use per person back towards those in the developed countries. Energy use per unit of industrial production within each technology is higher in China than in developed countries and will now gradually fall. The maturation of consumption will cause scrap to provide a gradually increasing proportion of metal requirements, reducing energy used in processing. These developments together with incentives to reduce greenhouse gas emissions hold out reasonable prospects for early stabilization and then reduction of industrial emissions, with some prospects of a peak before 2020 in the context of Chinese success with the new model of economic growth (Jiang 2014).

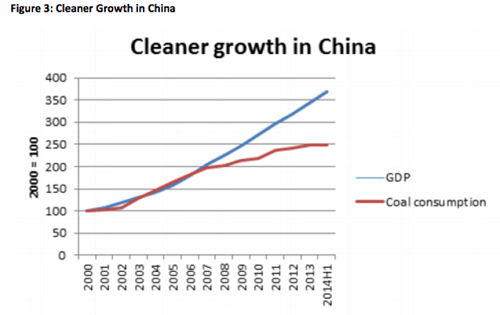

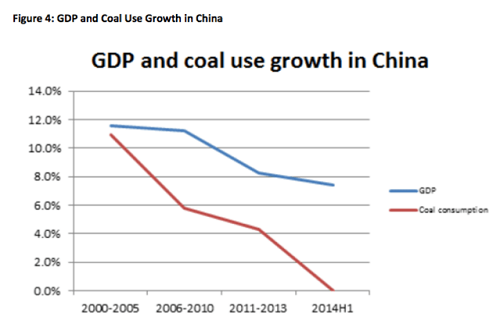

Declining coal use in industrial activity and the marked slowdown in growth of coal use in power generation are the main forces behind the decoupling of coal use from output growth that is already evident in the data (Figures 3 and 4).

Figures 3 and 4 Sources: Compiled from China National Bureau of Statistics and China National Coal Association statistical releases. Data from Justin Guay, Chinese Coal Consumption Just fell for the First Time This Century, reproduced in Renew Economy, 20 August 2014 http://reneweconomy.com.au/2014/chinese-coal-consumption-just-fell-for-first-time-this-century-49062

|

Figures 3 and 4 Sources: Compiled from China National Bureau of Statistics and China National Coal Association statistical releases. Data from Justin Guay, Chinese Coal Consumption Just fell for the First Time This Century, reproduced in Renew Economy, 20 August 2014 http://reneweconomy.com.au/2014/chinese-coal-consumption-just-fell-for-first-time-this-century-49062

|

Chinas contribution to low-carbon development in the developing world

Investment in research, development and commercialization of new technologies in the developed countries, especially the United States but also Germany, Japan and others, has extended the technological frontiers (U.S. Department of Energy 2013).

Chinas distinctive contribution has been to bring down the costs of manufacturing the capital goods embodying low emissions technologies through large scale deployment. This has occurred dramatically in photo voltaic panels, where manufacturing costs in some advanced Chinese plants have been reduced by 80 percent over half a dozen years. It has also been important for wind power generators, hydro-electric generators, battery storage and such energy saving devices as LED lighting instruments and high voltage electricity transmission.

Large scale manufacturing in China is in the process of bringing down costs radically for some major components of nuclear power generators, high speed rail and electric cars.

This is lowering the cost of reducing emissions all over the world. It is an important part of the reason why most countries are finding it easier and less costly to meet the Cancun mitigation targets than had been anticipated in early studies of the costs of avoiding dangerous climate change (Stern 2007; Garnaut 2008).

Most importantly of all, the reduction in costs of low emissions technologies is changing the technological choices available to countries in the early stages of modern economic development. It is holding out the prospects for the countries of South Asia and Africa moving directly to low emissions decentralized sources of electricity and transport, without having to dismantle investments in old technologies (Purohit, 2014).

China is demonstrating that it is now less costly to extend electricity to rural communities away from established grids through decentralized systems based on renewable hydro, solar, wind and biomass power. This example is already being influential in rural South Asia and Africa.

In India, for example, the costs of making electric power available to all villages is now likely to be lower through distributed renewable power generation than through huge, centralized and capital-intensive systems of generation and transmission. President Modi was elected in 2014 on a programme of rural electrification based on solar power following his success with such

policies at state level as Governor of Gujarat (Purohit, 2014). Developing countries at early stages of development are more aware than those that went before them of the domestic and international environmental costs of the old, centralized power systems based on fossil fuels.And the new alternatives make fewer demands on scarce engineering and management skills, the absence of which make the centralized, capital-intensive systems less reliable as well as more expensive than in their developed countries of origin.

Chinas contribution to introducing economically attractive alternatives to duplicating old emissions-intensive electricity, transport and industrial systems in the new developing countries may turn out to be as important to the global mitigation effort as the rapid change in the trajectory of its own emissions within the new model of economic growth.

Chinese diplomacy and the global mitigation effort

China has taken defensive diplomatic positions in early twenty first century meetings of the UNFCCC, as if its main objective were to avoid international pressure to reduce its own emissions. The success of Chinas new model of economic growth makes this approach at once unnecessary and wasteful. It is unnecessary because the new model of economic growth allows China to meet and to exceed any reasonable expectations for its own reductions in emissions. It is wasteful because the lowering of emissions growth trajectories within the new

model of economic growth allows China to put before the international community

commitments that can encourage greater ambition in reducing emissions in other countries.

In this context, Chinas participation in the Copenhagen meeting of the UNFCCC in 2009 represented lost opportunity for progress on global efforts to hold the human-induced increase in temperature to 2 degrees Celsius. Chinas commitment to reduce the emissions intensity of production by 40-45 percent between 2005 and 2020 represented a larger reduction in emissions from business as usual than any other national proposal. However, it was not presented this way by China, nor understood this way by other countries. Recognition of the significance of the Chinese commitment could have provided momentum for a successful outcome at Copenhagen. Instead, a false idea that China was not offering much was a drag on the meeting and contributed to diplomatic discord and a weak outcome.

The opportunity that success with the new model of economic growth provides for China further to reduce emissions growth trajectories by large amounts is a new opportunity for lifting the global mitigation effort.

Chinas successful delivery of its Cancun commitments to reduce emissions intensity by 40-45 percent itself makes a large contribution to the global mitigation effort. The confident prospects for extending success so far with the new growth model into further reductions in coal based electricity generation and industrial production allow China to extend its commitments on reducing emissions. There would be little risk in China committing to hold emissions from electricity generation to levels no higher than the highest reached in any year

up to 2015. I have not done the work confidently to justify similar statements about commitments on emissions from other sectors, and additional research would need to be commissioned by the Chinese authorities before additional commitments were placed before the international community. However, I would not be at all surprised if that extra work confirmed the prudence of an additional commitment to reach a peak in the absolute level of emissions by 2020.

Strong commitments by China at the Paris meeting of the UNFCCC in 2015 would transform the global discussions of the 2 degree objective. It would be transformative for China to unt to do its best to hold emissions at peaks in 2015 for electricity generation and 2020 for all activities. This would not be a legally binding international commitment, as such commitments are not the basis of the country pledges for 2020 and are unlikely to be the basis of an agreement in Paris for emissions reductions 2020-30. But it would be a serious domestic

political commitment, as the pledge on emissions intensity have been. This transformation of international ambition in climate change mitigation would be secured at little risk of underperformance, or of high costs.

Strong commitments by China at the Paris meeting of the UNFCCC in 2015 would transform the global discussions of the 2 degree objective. It would be transformative for China to undertake to do its best to hold emissions at peaks in 2015 for electricity generation and 2020 for all activities. This would not be a legally binding international commitment, as such commitments are not the basis of the country pledges for 2020 and are unlikely to be the basis of an agreement in Paris for emissions reductions 2020-30. But it would be a serious domestic political commitment, as the pledge on emissions intensity have been. This transformation of international ambition in climate change mitigation would be secured at little risk of underperformance, or of high costs.

The decisive fall in the trajectory of Chinese emissions growth since 2011 within a new model of economic development has brought within reach the possibility of holding human-induced increases in temperature to 2 degrees Celsius. It is crucial for the global mitigation effort that these developments in China are brought to account in the UNFCCC meeting in Paris in December 2015, which will discuss the basis for global cooperation 2020-2030. It is crucial to

the global mitigation effort that Australia and other countries respond to the developments in China with ambitious extensions of their own efforts to reduce greenhouse gas emissions.

References

Cai, F. 2014, Beyond Demographic Dividends, World Scientific and China Social Sciences, Academic Press, Singapore and Beijing.

Chen, Y.Y., A. Ebenstein, M. Greenstone and B.H. Li 2013. Evidence on the impact of sustained exposure to air pollution on life expectancy from Chinas Huai River policy, Proceedings of National Academy of Sciences of the US, July 8, Beijing.

Citibank 2013, The Unimaginable: Peak Coal in China, Research Report, 4 September 2013.

Dupont, A. and Pearman, G. 2006, Heating up the Planet: climate change and security, Lowy Institute Paper 12.

Garnaut, R. 2008, The Garnaut Climate Change Review, Cambridge University Press, Melbourne; Chinese language edition published by China Social Sciences Academic Press, Beijing.

Garnaut, R. 2014 forthcoming, Energy Policy in an Era of Carbon Constraints, Australian Economic Review.

Garnaut, R., F. Cai and L. Song (editors) 2013, China: A New Model for Growth and Development, Australian National University E-Press, Canberra, co-published with the China Social Sciences Academic Press; Chinese language edition published by China Social Sciences Academic Press, Beijing.

Guay, J. 2014 Chinese Coal Consumption Just fell for the First Time This Century, reproduced

in Renew Economy, 20 August 2014.

International Energy Agency 2013, World Energy Outlook 2013, OECD/IEA, Paris.

International Energy Agency, China Data Base, OECD/IEA, Paris.

IPCC (Inter-governmental Panel on Climate Change) 2007, Third Assessment Report, Cambridge and New York.

Jiang, K. 2014, Chinas CO2 Emission Scenario Toward 2 Degree Global Target, presentation to

Victoria University conference Abrupt change in Chinas energy path: implications for China,

Australia and the global climate.

Mai, Y. and S. Feng 2013, Increasing Chinas Coal-based Power Generation Efficiency: The Impact on Carbon Intensity and the Broader Chinese Economy to 2020, paper to the National Development and Reform Commission (State Information Center) Workshop, Beijing.

Peoples Republic of China, 2011, 12th Five-Year Plan (in Chinese).

Purohit, P. 2014 Increase in coal tax will scale up Indian renewables East Asia Forum, 20 August.

Sheehan, P., E. Cheng, A. English and F. Sun, 2014, Chinas response to the air pollution shock, Nature Climate Change, 4, 306-309.

Song, L., R. Garnaut and F. Cai (editors) 2014, Deepening Reform for Chinas Long-Term Growth and Development, Australian National University E-Press, Canberra.

Stern, N.H. 2007, The Economics of Climate Change: The Stern Review, Cambridge University Press, Cambridge, MA.

U.S. Department of Energy, 2013, Wind Power Costs Near Record Low, 6 August, Washington DC.

ABOUT THE AUTHOR

Ross Garnaut is a Professorial Research Fellow in Economics at University of Melbourne. He is affiliated with the Garnaut Climate Change Review and the Garnaut Climate Change Review Update 2011.

|

![[groups_small]](groups_small.gif)