Checking on the Limits to Growth

With over forty years of hindsight available since The Limits to Growth (LTG) was first published

(Meadows et al., 1972, Meadows et al., 1974), it is timely to review how society is tracking relative

to their ground-breaking modelling of scenarios, and to consider whether the global economy and

population is on a path of sustainability or collapse. Over a similar timeframe, international efforts

based around a series of United Nations (UN) conferences have yielded mixed results at best (Linner

and Selin, 2013, Meadowcroft, 2013). In addition to unresolved critical environmental issues and

resource constraints such as anthropogenic climate change and peak oil, the global economy is also

beset by ongoing challenges from the Global Financial Crisis (GFC), not least of which are lingering

levels of extraordinary debt. The standard political remedy of growing the economy out of debt has

potential ramifications for environmental stability, with evident negative feedbacks on the economy.

The intertwined economy-environment dependencies embodied in the original 1970s LTG modelling

provide an opportunity to examine how the global predicament has unfolded and what it might

mean for the future.

Through a dozen scenarios simulated in a global model (World3) of the environment and economy,

Meadows et al. (1972, p. 125) identified that overshoot and collapse was avoidable only if considerable

change in social behaviour and technological progress was made early in advance of environmental

or resource issues. When this was not achieved in the simulated scenarios, collapse of the

economy and human population (ie. a relatively rapid fall) occurred in the 21st century, reducing

living conditions to levels akin to the early 20th century according to the modelled average global

conditions. Exactly how this would play out in the real world is open to conjecture, as noted below.

Despite the LTG initially becoming a best-selling publication, the work was subsequently largely

relegated to the dustbin of history by a variety of critics (eg., Lomborg and Rubin, 2002). These

critics perpetuated the public myth that the LTG had been wrong, saying that it had forecast collapse

to have occurred well before year 2000 when the LTG had not done this at all. Ugo Bardis

The Limits to Growth Revisited (2011) comprehensively details the various efforts to discredit the LTG

study. He draws parallels with documented campaigns against the science of climate change and

tobacco health impacts. Three economists- Peter Passel, Marc Roberts, and Leonard Ross- initiated

criticisms in a New York Times Sunday Book Review article in 1972. They made false statements (eg.

all the simulations based on the Meadows world model invariably end in collapse), and also incorrectly

claimed that the book predicted depletion of many resources by about 1990. The US economist

William Nordhaus made technically erroneous judgements (in 1992) by focusing on isolated

equations in World3 without considering the influence that occurs through the feedbacks in the

rest of the model. In 1973 a critique of the LTG, edited by physicist Sam Cole and colleagues at the

University of Sussex, contained a technical review of the World3 modelling and essays based on

ideology that attacked the authors personally. According to Bardi, the technical review fails because

it largely concerned how the World3 model could not be validated from the perspective of simple

linear modelling, which is an inappropriate test for a non-linear model. The review also established

that the model could not run backwards in time, though this is an unnecessary requirement for the

model to run forward properly. Criticism of the study continued for about two decades, including

other noted economists such as Julian Simon, along the vein of such misunderstandings and personal

attacks. For the last decade of the twentieth century, however, criticism of the LTG centred on

the myth that the 1972 work had predicted resource depletion and global collapse by the end of

that century. Bardi identifies a 1989 article titled Dr. Doom by Ronald Bailey in Forbes magazine

as the beginning of this view. Since then it has been promulgated widely, including through popular

commentators such as the Danish statistical analyst Bjørn Lomborg, and even in educational texts,

peer-reviewed literature, and reports by environmental organisations.

Over the last decade, however, there has been something of a revival in awareness and understanding

of the LTG. Most recently, Randers (2012a)a LTG co-authorhas published his forecast of the

global situation in 2052 and renewed the lessons from the original publication (Randers 2012b).

A turning point in the debate occurred in 2000 with the energy analyst Simmons (2000) raising

the possibility that the LTG modelling was more accurate than generally perceived. Others have

made more comprehensive assessments of the model output (Hall and Day, 2009, Turner, 2008);

indeed, my earlier work found that thirty years of historical data compared very well with the LTG

standard run scenario. The standard run scenario embodies the business-as-usual (BAU) social

and economic practices of the historical period of the model calibration (1900 to 1970), with the

scenario modelled from 1970 onwards.

This paper presents an update on the prior data comparison by Turner (2008). An update is especially

pertinent now because of questions raised about how the current economic downturn

commonly associated with the GFCmay relate to the onset of collapse in the LTG BAU scenario.

Is it possible that aspects leading to the collapse in the LTG BAU scenario have contributed to the

GFC-related economic downturn? Could it be that this downturn is therefore a harbinger of global

collapse as modelled in the LTG?

To provide context and convey the importance of understanding global dynamics, this paper first

summarises the mechanisms that play-out in the modelled BAU scenario. Subsequently, the modelled

trajectory is compared with some forty-years of historical data (which are outlined in the appendix).

The appendix also provides comparison of the data with two other scenarios, namely comprehensive

technology and stabilized world scenarios (with full details in Turner, 2012)showing

that the comparison strongly favours the BAU scenario only. On the basis of this comparison, we

discuss what the modelling might mean for a resource-constrained global economy. In particular, the

paper examines the issue of peak oil and the link between energy return on investment (EROI) and

the LTG World3 model. The findings lead to a discussion of the role of oil constraints in the GFC,

and a consideration of the link between these constraints and general collapse depicted in the LTG.

This paper does not attempt to deal with the critical but vexed issue of appropriate governance;

other research is shedding light on the difficulties thwarting change (eg. Harich, 2010, Rickards et

al., 2014). Instead, it aims to forewarn of potential global collapseperhaps more imminent than

generally recognisedin the hope that this may spur on change, or at least to prepare readers for a

worst case outcome.

Modelling future worlds

The computer model called World3, developed for the LTG study, simulated numerous interactions

within and among the key subsystems of the global economy: population, industrial capital, pollution,

agricultural systems, and non-renewable resources. For its time, World3 was necessarily coarse, for

example modelling the total global population rather than separate regions or nations. In the system

dynamics approach, causal links were made mathematically to reflect the influence of one variable

on another (not necessarily in a linear fashion), both within and between various sectors of the

global economic system. In this way, positive and negative feedback loops were established, where

the outcome in one part of the system subsequently returns by a chain of influences to affect itself.

When positive and negative feedback loops are finely balanced, a steady state outcome results (or

oscillations about an average); however, when one loop dominates, an unstable state is the result,

such as the simple case of exponential growth when there is a dominant positive feedback. A classic

example is the accelerating growth of a biological population, such as bacteria, in which the birth

rate at one point in time is proportional to the size of the population at that time.

The effect and control of these feedbacks depends on the presence of delays in the signals from

one part of the world system to another. For instance, the effects of increasing pollution levels on

human life expectancy or agricultural production may not be recognised for some decades after

the pollution is emitted. This is important because unless the effects are anticipated and preventive

action taken in advance, the increasing levels of pollutants may grow to an extent that prohibits correction.

These are the dynamics that lead to overshoot and collapse.

The World3 model simulated a stock of non-renewable as well as renewable resources. The function

of renewable resources in World3, such as agricultural land and the trees, could erode as a

result of economic activity, but they could also recover their function if deliberate action was taken

or harmful activity reduced. The rate of recovery relative to rates of degradation affects when

thresholds or limits are exceeded as well as the magnitude of any potential collapse.

To explore the broad behaviour modes of the population-capital system (Meadows et al. 1972, 91)

the LTG presented a dozen scenarios exploring the effects of various technological improvements

and societal or policy changes. The scenario series started with a standard run which encapsulated

business-as-usual (BAU) values in the model for the future. Parameter trends for this scenario

were based on historical data and behaviour (established to reproduce approximately the growth

and dynamics observed from 1900 to 1970).

Impending collapse of the BAU scenario

As described below, data from the forty years or so since the LTG study was completed indicates

that the world is closely tracking the BAU scenario. In the BAU, during the 20th century increasing

population and demand for material wealth drives more industrial output, which grows at a faster

rate than population. Pollution from increasing economic activity increases, but from a very low

level, and does not seriously impact the population or environment.

However, the increased industrial activity requires ever increasing resource inputs (albeit offset by

improvements in efficiency), and resource extraction requires capital (machinery) which is produced

by the industrial sector (which also produces consumption goods). Until the non-renewable

resource base is reduced to about 50 per cent of the original or ultimate level, the World3 model

assumed only a small fraction (5 per cent) of capital is allocated to the resource sector, simulating

access to easily obtained or high quality resources, as well as improvements in discovery and

extraction technology. However, as resources drop below the 50 per cent level in the early part of

the simulated 21st century and become harder to extract and process, the capital needed begins to

increase. For instance, at 30 per cent of the original resource base, the fraction of total capital that

is allocated in the model to the resource sector reaches 50 per cent, and continues to increase as

the resource base is further depleted (shown in Meadows et al., 1974).

With significant capital subsequently going into resource extraction, there is insufficient capital

available to fully replace degrading capital within the industrial sector itself. Consequently, despite

heightened industrial activity attempting to satisfy multiple demands from all sectors and the

population, actual industrial output (per capita) begins to fall precipitously from about 2015, while

pollution from the industrial activity continues to grow. The reduction of inputs to agriculture from

industry, combined with pollution impacts on agricultural land, leads to a fall in agricultural yields

and food produced per capita. Similarly, services (eg. health and education) are not maintained due

to insufficient capital and inputs.

Diminishing per capita supply of services and food causes a rise in the death rate from about 2020

(and a somewhat lower rise in the birth rate, due to reduced birth control options). The global

population therefore falls, at about half a billion per decade, starting at about 2030. Following the

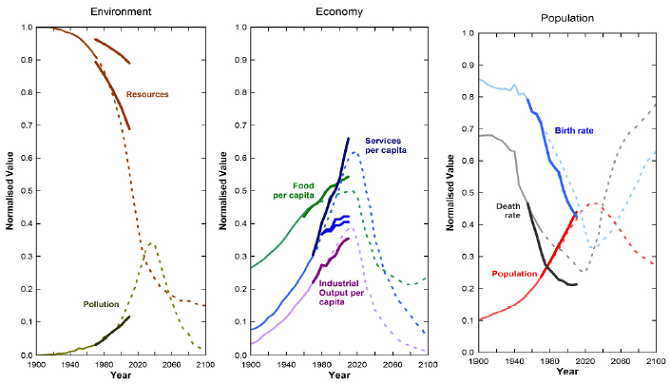

collapse, the output of the World3 model for the BAU (Figure 1) shows that average living standards

for the aggregate population (material wealth, food and services per capita basically reflecting

OECD-type conditions) resemble those of the early 20th century.

The implications of the BAU scenario are stark: Figure 1 depicts global collapse of the economic

system and population. Essentially this collapse is caused by resource constraints (Meadows et al.,

1972), following the dynamics and interactions described above. The calibrated dynamics reflect

observed responses within the economy to changing levels of abundance or scarcity (Meadows et

al., 1974), obviating the need for modelling prices as the communication channel of the economic

responses.i

The LTG Business As Usual scenario tracks reality

With forty years passing since the original LTG modelling, it is opportune to examine how well the

scenarios reflect reality. In this section a graphical comparison is presented of the historical data

with the BAU scenario described above (Figure 1). It is evident from Figure 1 that the data generally

aligns strongly with the BAU scenario (for most of the variables); while the data does not align

with the other two scenarios (Turner, 2012, Turner, 2008) (see Appendix 1).

The demographic variables displayed in Figure 1 continue to show the same comparisons as seen

in the thirty year review (Turner, 2008), so that population would peak somewhat higher than the

BAU by 2030, or later according to an extrapolation of the difference between the birth and death

rates. It is more evident now, however, that the crude death rate has leveled off while the birth

rate continues to fall, which are general trends seen in the three scenarios, albeit at different values.

Notably, the death rate reverses its monotonic decline and begins to climb in all scenarios within a

decade; significantly so in the standard run (and comprehensive technology) scenario by 2020.

Outputs of the economic system (Figure 1) show trends mostly commensurate with the LTG

BAU. Importantly, any downturn in industrial activity due to the GFC has not been captured in the

historic data since these were only available to 2007. Nevertheless, the observed industrial output

per capita illustrates a slowing rate of growth that is consistent with the BAU reaching a peak. In

this scenario, the industrial output per capita begins a substantial reversal and decline at about 2015.

Observed food per capita is broadly in keeping with the LTG BAU, with food supply increasing only

marginally faster than population. Literacy rates show a saturating growth trend, while electricity

generation per capita (upper data curve) grows more rapidly and in better agreement with the LTG

model (Figure 1).

Global pollution measured by CO2 concentration is most consistent with the BAU scenario (Figure

1), but this ten year data update indicates that it is rising at a somewhat slower rate than that modelled.

This could be due to a number of factors, which cannot be separately identified in this analysis.

For instance, in comparison with the BAU model output, lower observed industrial output per

capita is consistent with lower observed pollution generation, though this effect will be offset by the

slightly higher observed population levels. It is also possible that the dynamics of persistent pollution

generation by different economic activities or assimilation in the environment are not parameterized

in the World3 model precisely in terms of actual CO2 dynamics (which is still a topic of active

research). In this possibility, the recent data are consistent with a slightly higher assimilation rate, or

alternatively, a lower pollution generation rate in the agriculture sector compared with the industrial

sector (since the relative rate of food production is greater than industrial output).

Figure 1. LTG BAU (Standard Run) scenario (dotted lines) compared with historical data from 1970 to 2010 (solid lines)for demographic variables: population, crude birth rate, crude death rate; for economic output variables: industrial output per capita, food per capita, services per capita (upper curve: electricity p.c.; lower curves: literacy rates for adults, and youths [lowest data curve]); for environmental variables: global persistent pollution, fraction of non-renewable resources remaining (upper curve uses an upper limit of 150,000 EJ for ultimate energy resources; lower curve uses a lower limit of 60,000 EJ [Turner 2008]).

|

Regardless of the explanation, the level of global pollution is sufficiently low (in all scenarios, and the

data) to not have a serious impact on the environment and human life-expectancy (Turner, 2008).

In contrast, of the two data curves of non-renewable resources remaining, the lower estimate

demonstrates a closer alignment with the BAU (while the upper estimate aligns well with the comprehensive

technology scenario [Figure 1]). The lower estimate also shows a significant fall toward

the point when the World3 model incorporates a growing diversion of capital toward the resource

sector in order to extract more difficult resources (5060 per cent of the original resource; see

Meadows et al., 1974, figure 5-18). This is the primary cause of collapse in the BAU scenario, as

described above. The observed data is based on energy resources (see discussion in Turner 2008,

pp. 405-407), conservatively assuming full substitution potential among the different primary energy

types. This assumption may not be entirely accurate (for instance, in the case of transport fuels (primarily

oil) essential for the smooth functioning of the economy). Subsequent sections reflect upon

this question further.

Confidence through calibration

The striking comparison described above indicates that the original LTG work should not be dismissed

as many critics have attempted to do, and increases confidence in the LTG scenario modelling.

It is notable that there does not appear to be other economy-environment models that have

demonstrated such comprehensive and long-term data agreement. Nevertheless, this agreement is

not a complete validation of the model (partly due to the non-linear nature of the World3 model)

or the BAU scenario. Achieving validation requires at least that key inputs and non-linear (or

threshold) assumptions also be verified. This verification is partially initiated below with an examination

of the imposts of resource extraction.

Despite the non-linearity of the World3 model, the general outcomes of the scenarios are not

sensitive to reasonable uncertainties in key parameters (Meadows et al., 1974). Nevertheless, critics

continue to question the value of the LTG modelling based on perceived model sensitivity (Castro,

2012). Superficially, early sensitivity analysis of the World3 model (de Jongh, 1978, Vermeulen and de

Jongh, 1976) appeared to show that the model is sensitive to parameter changes. For example, by

imposing a 10 per cent change from 1970 onwards to three parameters in the industrial sector it

is possible to alter significantly the trajectories of the World3 output. In reproducing this change, I

found that the outcome was not avoidance of overshoot and collapse, contrary to the critics claim

(Turner, 2013). Instead, a wider examination of outputs indicates that overshoot and collapse was

simply delayed, and that the underlying reason for this was that industrial output per capita (a proxy

for material wealth) remained constant for decades before declining. In effect, the critics were actually

creating elements of the stabilized world scenario where material consumption was restrained,

but they did not acknowledge this.

Further, claims of parameter sensitivity evidently contradict the forty year alignment of the LTG

model with independent data; if the model was over-sensitive it should not successfully forecast

outcomes. The key to resolving this apparent paradox is to recognise that the World3 model was

calibrated as a whole system against data and trends from 1900 to 1970. This calibration is not simply

inferring parameter values from the available datawhich is recognised by everyone including

the LTG authors to incorporate sizable uncertaintiesbut more importantly that the various model

outputs (population, food, resources, etc.) must simultaneously produce reasonable values against

observed data. One sub-system of the model may work as an effective check on other sub-systems.

The whole-system calibration then constrains the collected values that parameters can have. This is

not to say that any single parameter is now known more accurately, which they are not. Rather, it is

the collection of interactions that matters. This is a key point that Bardi (2011) makes in his review

of earlier criticisms of the LTG (ie. the importance of treating a system as a whole and not isolating

sub-systems without reference to the rest of the system).

Additionally, there are general principles of control systems which apply despite parameter sensitivity

or uncertainty around the specifics of future system trajectories. It is a general property of

systems with self-reinforcing and self-correcting mechanisms (ie. positive and negative feedbacks, the

former producing growth) that they will overshoot their long-term equilibrium if there are sufficient

delays in recognising or responding to the negative signals. Should this be the case, it is inevitable

that the system will correct by falling or collapsing below that equilibrium.

Is collapse likely, and imminent? Examining mechanisms behind the near-term BAU collapse

Based simply on the comparison of observed data and the LTG scenarios presented above, and given

the significantly better alignment with the BAU scenario than the other two scenarios, it would

appear that the global economy and population is on the cusp of collapse. This contrasts with other

forecasts for the global future (eg. Raskin et al., 2010, Randers, 2012), which indicate a longer or

indeterminate period before global collapse; Randers for example forecasts collapse after 2050,

largely based around climate change impacts, with features akin to the LTG comprehensive technology

scenario. This section therefore examines more closely the mechanisms behind the near-term

BAU collapse and explores whether these resemble any real-world developments.

Real world developmentsPeak Oil

Having confirmed the significant alignment of 40 years of data with the BAU scenario, and established

that the model is not inappropriately sensitive, this section now considers whether the key

dynamics underlying the breakdown described above resemble actual developments. Since the collapse

in the BAU scenario is predominantly associated with resource constraint and the diversion

of capital to the resource sector, it is pertinent to examine peak oil (or other resource peaks). Peak

oil refers to the peak in production of oil (particularly from conventional supply), as opposed to

demand which is generally assumed to increase. Publications on peak oil have flourished in recent

years as the possibility of a global peak has become more widely accepted (eg. by the otherwise

conservative International Energy Agency) (Alexander, 2014). These publications tend to focus

on the question of when the peak will occur and what the oil supply volume will be. Sorrel et al.

(2010a, 2010b) review many of these and find that independent researchers generally expect peaking

to occur within about a decade, or to have occurred recently (Sorrell et al. 2010a, Sorrell et al.

2010b, Murray and King, 2012); estimates of peaking made by oil industry representatives tend to be

decades away. Unfortunately, these oil production profiles themselves say little analytically about the

implications of reduced oil supply rates on the economy, though qualitatively a constrained supply

of ubiquitous transport fuel is likely to be deleterious to the global and national economies (Hirsch,

2008, Friedrichs, 2010).

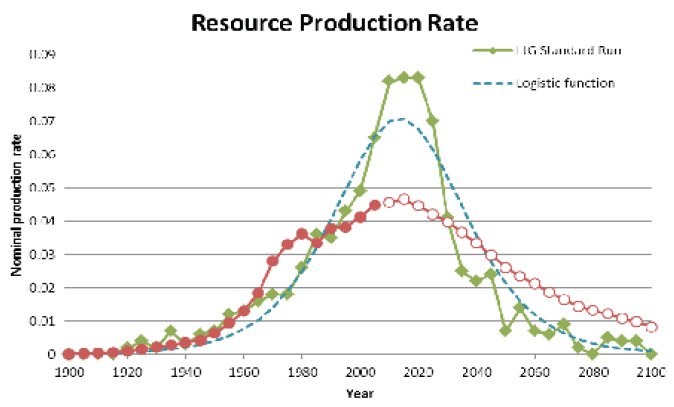

It is useful to compare the general qualities of past and future oil production with that inferred

from the LTG BAU output (Figure 2), even though there is inevitable uncertainty around individual

forecasts of oil production. The LTG production rate was derived by taking the first derivative of the

non-renewable resource data.

The LTG curve approximates a Hubbert-like profile, depicted in Figure 2 using a logistic function

(normalised to the same cumulative production ie. area under the curve). Hubbert assumed

a finite resource, with exponential growth in production in the early production phase (based on

data trends), and some mimic of discovery rates (ie. peaking and decline) leading eventually to zero

production (Hubbert, 1956). He originally drew arbitrary curves based on postulating peak production

rates, and estimates of ultimate resource. Subsequently, Hubbert used the more mathematically

convenient logistic function (for cumulative production) to capture the qualitative properties of

production profiles (Hubbert, 1982).

In comparison, oil production rates from actual and projected data do not peak and fall so rapidly,

although the data superficially indicate a much lower peak as a result of the accelerated production

or earlier peak between 1960 and 1985. The extra production (relative to LTG) in this period

very closely matches the deficiency in production (relative to LTG between 1990 and 2005). Indeed,

the cumulative production at 2005 is just 1 per cent different. The projection of oil production is

based on an empirical model of production lagging discovery (Gargett and BITRE, 2009), where

cumulative production cannot be greater than cumulative discoveries. Therefore, if discoveries have

peaked and fallen, production must also do so, though the actual rates can of course differ. It takes

no account of the how demand might vary, in contrast to the LTG.

Figure 2. Oil production rate: actual and projection; derived from the LTG; and a Hubbert-like curve based on a logistic function - all normalised to equal total resource (ie. area under the curves).

|

Unlike other projections of oil production, the LTG curve is not hardwired explicitly in the model,

but is an outcome of other dynamics. Exponential growth occurs initially because of the demand

from exponentially growing industrial activity. Production subsequently falls due to the collapse in

demand from industrial activity (see next section). Production of non-renewable resources in the

World3 model scales with population using a per capita resource usage multiplier, and the latter

is an increasing (approximately linear) function of industrial output per capita. Consequently, the

production rate follows the industrial output.

Notably the oil resource has not run out when the global collapse begins; far from it, since the peak

extraction rate occurs about halfway through the resource pool. Further, as respected commentators

(The Economist and The Guardian) point out, there are immense additional pools of fuels in the

form of unconventional oil and gas reserves, such as those being accessed by hydraulic fracturing

(fracking) (Maugeri, 2012). (These additional reserves were included in the data of non-renewable

resources for the comparison shown in Figure 1). The optimistic view being expressed recently

is that there could be a new oil and gas glut. This superficially appears to contradict the resource

constraint that underpins the collapse in the BAU scenario of the LTG.

But the protagonists of oil and gas gluts have not understood a crucial point. They have essentially

confused a stock with a flow. The key, as the LTG modelling highlights, is the rate at which the resource

can be supplied, ie. the flow, and the associated requirements of machinery, energy and other

inputs required to achieve that flow. Contemporary research into the energy required to extract

and supply a unit of energy from oil shows that the inputs have increased by almost an order of

magnitude. It does not matter how big the resource stock is if it cannot be extracted fast enough or

other scarce inputs needed elsewhere in the economy are consumed in the extraction. Oil and gas

optimists note that extracting unconventional fuels is only economic above an oil price somewhere

in the vicinity of US$70 per barrel. They readily acknowledge that the age of cheap oil is over, without

apparently realising that expensive fuels are a sign of constraints on extraction rates and inputs

needed. It is these constraints which lead to the collapse in the LTG modelling of the BAU scenario.

The end of easy oil, and subsequent global collapse

Consequently, what is more relevant than the oil supply rates per se to our analysis of the LTG and

collapse is the opportunity cost associated with extracting diminishing supplies of conventional oil

or difficult extraction of non-conventional oil (eg. tar sands, deep water, coal-to-liquids, etc.) (Murray

and King, 2012). In the LTG, the fraction of capital allocated to obtaining resources (FCAOR)

represents this opportunity cost. In the peak oil literature, the relevant measure of opportunity

cost is the energy return on investment (EROI) which is related to the net energy available after

energy is used extracting the resource (Heun and de Wit, 2012, Dale et al., 2011, Heinberg, 2009,

Murphy and Hall, 2011). The EROI is defined as the ratio of gross energy produced, TEProd, to energy

invested to obtain the energy produced, ERes.

The EROI can be related to the FCAOR used in the LTG. Since the capital (machinery eg., pumps,

vehicles) operated in the resource sector, CRes, is basically representative of the overall machinery

stock, CTtl, the energy intensities will be similar and therefore the ratio of capital can be approximated

by the ratio of energy used in the resource sector, ERes, to total energy consumed, TECons.

Since the total energy consumed in any year will be approximately equal to the total energy produced

(because stocks of energy stored are relatively small and dont change significantly from year

to year) TECons TEProd, then equations 1 and 2 give:

The collated data and model of EROI in Dale et al. (2011) can therefore be converted to FCAOR at

corresponding values for the fraction of the oil resource remaining. This can be then be compared

against the data used in the LTG (eg. shown in Meadows et al., 1974, figure 5-18). If the peak of

conventional oil has occurred, or is about to occur, then approximately half the resource has been

consumed, ie. non-renewable resource fraction remaining, NRFR 0.5. Contemporary estimates of

EROI are in the range 10-20 (or 1/EROI of 0.1-0.05). This agrees with the values and trends of the

key parameter, FCAOR, used in the LTG (see Figure 3).

Therefore, in addition to the data comparison made for modelled outputs, this data on oil resource

extraction corroborates a key driver of dynamics in the LTG BAU scenario. In other words, in addition

to outputs of the model aligning with data, the key mechanism driving the collapse in the BAU

is also observed in real world data.

The limited role of alternative energy innovation

Given that the key mechanism underlying collapse in the BAU scenario is evidently the diversion

of capital toward extracting depleting resources, it is pertinent to examine the sensitivity of the

scenario to changes in this factor. In the case of oil (and gas) resources in particular, could it be that

the current expansion of unconventional resources (tight oil, shale oil and gas, tar sands, etc.) is sufficient

to offset the decline in production of conventional oil? Critics of unconventional resources

point toward decreasing net energy due to the difficulty of extraction. In terms of the LTG modelling,

this relates to the fraction of capital allocated to obtaining resources (FOCAR) increasing as

the resource stock reduces (such as in the BAU setting). However, it is early days in the new play of

unconventional resources, so it would be reasonable to anticipate that cumulating experience and

new technologies will ease the extraction task and hence reduce the energy/capital required for

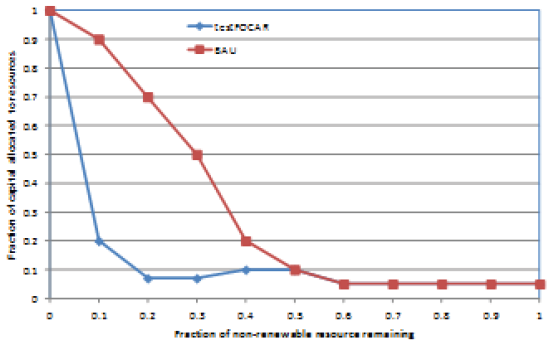

each barrel of oil. This possibility has been tested in the World3 model, using the setting (testFOCAR)

shown in Figure 3.

Figure 3. Increased efficiency in extraction of unconventional resources (blue curve) as the fraction of resource declines toward zero, compared with the BAU setting (red).

|

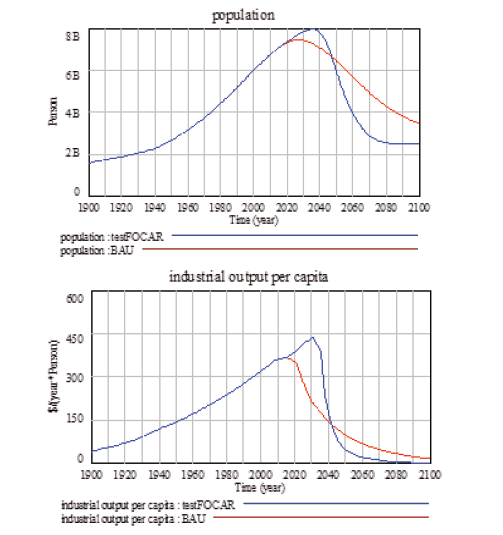

Figure 4. Collapse delayed by about 2 decades, but is worse (ie. a Seneca cliff), due to increased efficiency in accessing unconventional resources.

|

The alternative FOCAR is held at current levels and even slightly decreased (to half-way between

the original 5 per cent and current level) to simulate the effect of cost saving technologies. But as

the resource remaining approaches 10 per cent, the extraction effort increases and must approach

a FOCAR of 1 as the resource is exhausted (the value of 1 actually prevents the non-renewable

resource from being completely exhausted because the economic costs of harvesting resources effectively

slows the resource extraction rate). This type of FOCAR was also tested by the LTG team

(see pp. 398405 Meadows et al., 1974) among other sensitivity tests.

However, collapse is not avoided but simply delayed by one to two decades (Figure 4), and when

it occurs the speed of decline is even greater. Easier to obtain resources permit economic growth

to be re-kindled following a relatively minor hiatus at about 2015. Subsequently, the draw-down of

non-renewable resources continues apace, and reaches such a low level that the industrial system

cannot be supported and output drops rapidly at about 2030. As a result, population grows a little

higher than the BAU, but falls from about 2035 at a faster rate and to a lower level.

Contemporary impacts of oil constraints: is collapse underway?

The close alignment between the LTG BAU scenario and observed developments over the last four

decades, as well as the correspondence in the underlying dynamics described above, portend of potential

global collapse. Although the general commentary on the LTG describes collapse occurring

sometime mid-century (and the LTG authors stressed not interpreting the time scale too precisely),

the BAU scenario implies that a relatively rapid fall in economic conditions and the population

could be imminent. Indeed, other aspects of oil supply constraints explored in the following, indicate

that the ongoing economic downturn of the GFC may be representative of an imminent BAU style

collapse.

Firstly, oil price rises have been linked to recent increases in food prices (eg. (Alghalith, 2010, Chen

et al., 2010). There are direct and indirect links between oil and food (Schwartz et al., 2011, Neff

et al., 2011), associated with fuel for machinery and transport, both on-farm and in processing and

distribution, as well as feedstock for inputs such as pesticides. Also, although nitrogen fertilizer is

largely manufactured from natural gas, the price of these commodities is also linked to that of oil.

More recently, production of bio-fuel as an alternative transport fuel, such as corn-based ethanol,

has displaced food production and has been a factor in food price increases (eg. Alghalith, 2010,

Chen et al., 2010). These developments resemble the dynamics in the LTG BAU scenario where

agricultural production is negatively affected by reduced inputs. There may also be evidence of global

pollution beginning to impact food production (which is a secondary factor in the BAU scenario) in

the recent occurrence of major droughts, storms and fires (eg. Russia, Australia) that are potentially

early impacts of global climate change driven by anthropogenic greenhouse gas emissions.

The role of oil (and food) prices extends further, into more general economic and political shocks.

For instance, other aggregate modelling of the role of energy in the economy (Nel and Cooper,

2009) finds that energy constraints cause a long-term economic downturn, as well as reducing

greenhouse gas emissions, which are similar outcomes to those in the LTG collapse. Empirically,

there is clear evidence (eg. Murray and King, 2012, overviews in Murphy and Hall, 2010, Murphy

and Hall, 2011) of a connection between many oil price increases and economic recessions (just as

there exists a strong correlation between energy consumption and growth in economic indicators).

Hamiltons econometric analysis (2009) indicates that the latest (US) recession, associated with the

GFC, was different from previous oil-related shocks in that it appears caused by the combination of

strong world demand confronting stagnating world production. His analysis downplays the role of

financial speculation.

Nevertheless, the overriding proximate cause of the GFC is evidently financial: excessive levels of

debt (relative to gross domestic product (GDP), or more accurately, the actual capacity of the real

economy to pay back the debt) (Keen, 2009). Such financial dynamics were not incorporated in the

LTG modelling. Das (2011) highlights correlated defaults in high-risk debts, such as sub-prime housing

mortgages, as a key trigger of the GFC. The financial models used did not properly account for

a high number of defaults occurring simultaneously, being based on statistical analysis from earlier

periods which suggest less correlation in defaults. Correlation may be caused by specific aspects

of the financial instruments created recently, including for example, adjustments upward in interest

rates of sub-prime mortgages after an initial teaser period of negligible interest rates. Even so,

some spread in defaults would be expected in this case. Alternatively, another potential factor could

be the price increases in oil and related commodities, which would be experienced by all households

simultaneously (but with a disproportionate impact on large numbers of households with low

discretionary income) and hence cause the coordinated debt defaults.

Regardless of what role oil constraints and price increases played in the current GFC, a final consideration

is whether there is scope of a successful transition to alternative transport fuel(s) and

renewable energy more generally. Due to the GFC, there may be a lack of credit for funding any

coordinated (or spontaneous) transition (Fantazzini et al., 2011). And economic recovery may be

interrupted, repeatedly, by increased oil prices associated with any recovery. Additionally, even if

a transition is initiated it may take about two decades to properly implement the change over to

a new vehicle fleet and distribution infrastructure (Hirsch, 2008, Hirsch et al., 2005). To transition

requires introducing a new transport fuel to compensate for possible oil production depletion rates

of four per cent (or higher) while also satisfying any additional demand associated with economic

growth. It is unclear that these various conditions required for a transition are possible.

The role of social responses

In terms of social changes, it is pertinent to note that while the authors of the LTG caution that

the dynamics in the World3 model continue to operate throughout any breakdown, different social

dynamics might come to prominence that either exaggerate or ameliorate the collapse (eg. reform

through global leadership, regional or global wars). Other researchers have contemplated how

society might respond to serious resource constraints (eg. Friedrichs, 2010, Fantazzini et al., 2011,

Heinberg, 2007, Orlov, 2008, Heinberg, 2011). Various degrees of hostility are foreshadowed, as well

as lifestyles in developed countries that revert to greater self-reliance.

The dynamics in the World3 model leading to collapse resonate with aspects of other conceptual

accounts of failed civilizations (Tainter, 1988, Diamond, 2005, Greer, 2008, Greer, 2005). Tainters

proposition of diminishing returns from growing complexity relates to the increasing inefficiency of

extracting depleting resources in the World3 response. It also aligns with a more general observation

in the LTG that successive attempts to solve the sustainability challenges in the World3 model,

which lead to the comprehensive technology scenario, result in even more substantial collapse. The

existence in World3 of delays in recognising and responding to environmental problems resonates

with key elements in Diamonds characterisation of societies that have failed. And Greers mechanism

of catabolic collapse - ie. increases in capital production outstripping maintenance, coupled

with serious depletion of key resources - describes in a slower mode the core driver of breakdown

in the LTG BAU.

Unfortunately, scientific evidence of severe environmental or natural resource problems has been

met with considerable resistance from powerful societal forces, as the long history of the LTG and

international UN initiatives on environmental/climate-change issues clearly demonstrate. Somewhat

ironically, the apparent corroboration here of the LTG BAU implies that the scientific and public

attention given to climate change, whilst tremendously important in its own right, may have deleteriously

distracted from the issue of resource constraints, particularly that of oil supply. Indeed,

if global collapse occurs as in this LTG scenario then pollution impacts will naturally be resolved

though not in any ideal sense! A challenging lesson from the LTG scenarios is that global environmental

issues are typically intertwined and should not be treated as isolated problems. Another

lesson is the importance of taking pre-emptive action well ahead of problems becoming entrenched.

Regrettably, the alignment of data trends with the LTG dynamics indicates that the early stages of

collapse could occur within a decade, or might even be underway. This suggests, from a rational risk-

based perspective, that we have squandered the past decades, and that preparing for a collapsing

global system could be even more important than trying to avoid collapse.

Appendix

Updates to the historical data

The data presented here follows that of the thirty year review (Turner, 2008). This data covers the

variables displayed in the LTG output graphs: population (and crude birth and death rates); food supply

per capita; industrial output per capita; services per capita; fraction of non-renewable resources

available; and persistent global pollution. Data sources are all publically available, many of them

through the various United Nations organisations (and websites). Details were provided earlier

(Turner, 2008) on these data sources and aspects such as interpretation, uncertainties and aggregation.

However, some additional data and calculation were necessary since measured data to 2010

was not always available (and even when it is the data may be forecast estimates). A summary of the

data is provided in the following.

Population data is readily available from the Population Division of the Department of Economic

and Social Affairs of the UN (United Nations) Secretariat (obtained via the online EarthTrends

database of the World Resources Institute); but data from 2006 onwards is a forecast. Given the

short gap to 2010 and typical inertia in population dynamics, the 2010 estimate will be sufficiently

accurate for the comparison made here.

Food supply was based on energy supply data (calories) from the Food and Agriculture Organisation

(FAO), with the extension to 2009/10 generated from comparison with production data, which

was scaled to the energy supply data for each corresponding food type in the production data.

Industrial output was available only to 2007 directly from the UN Statistical Yearbooks (UN 2006,

2008), now accessible online. Industrial output per capita is used as a measure of material wealth in

the LTG modelling, but the industrial output also supplies capital for use in other sectors, including

agriculture and resource extraction.

Service provision (per capita) has been measured by proxy indicators: electricity consumed per

capita and literacy rates. In the former case, for the most recent data it was necessary to scale

electricity generation data (from BP Statistical Review 2011) to consumption values and hence

account for electricity transmission losses. Literacy rates were updated from the United Nations

Educational, Scientific and Cultural Organisation (UNESCO) Statistics database, which is the source

for the EarthTrends data. Literacy rates provide a partial proxy indicator since they will saturate as

they increase toward 100 per cent. Values are provided for time ranges rather than single years.

The fraction of non-renewable resources available is estimated from production data on energy

resources, since other resources are conservatively assumed to be infinitely substitutable or there

to be unlimited resources. Energy production data to 2010 was obtained from the BP Statistical

Review (2011), which was subtracted from the ultimate resource originally available to obtain the

remaining resources. To account for considerable uncertainty in the ultimate resource, upper and

lower estimates were made based on optimistic and constrained assessments, respectively (Turner,

2008). Hence, two data curves are provided for the fraction of non-renewable resources remaining.

Finally, global persistent pollution was measured by the greenhouse gas CO2 concentration, available

to 2008 on the EarthTrends database, with latest measurements to 2010 from Pieter Tans, National

Oceanic and Atmospheric Administration (NOAA) Earth System Research Laboratory (ESRL),

and Ralph Keeling, Scripps Institution of Oceanography.

Data comparison with three bounding scenarios

To help convey how significant is the strong alignment of data with the BAU or standard run scenario,

with this expands the comparison to two other key scenarios from the LTG modelling, namely

the comprehensive technology and stabilized world scenarios. The three scenarios together

effectively present a bounding envelope for the full spectrum of scenarios produced.

The comprehensive technology scenario attempts to solve sustainability issues with a broad range

of purely technological solutions. This technology-based scenario incorporates levels of resources

that are effectively unlimited, 75 per cent of materials are recycled, pollution generation is reduced

to 25 per cent of its 1970 value, agricultural land yields are doubled, and birth control is available

world-wide.

For the stabilized world scenario, both technological solutions and deliberate social policies are

implemented to achieve equilibrium states for key factors including population, material wealth,

food and services per capita. Examples of actions implemented in the World3 model include: perfect

birth control and desired family size of two children; preference for consumption of services

and health facilities and less toward material goods; pollution control technology; maintenance of

agricultural land through diversion of capital from industrial use; and increased lifetime of industrial

capital.

Notes

i One particularly important case in point is the change from elastic to inelastic supply of oil and

the resulting economic implications (Murray and King, 2012, Murray and Hansen, 2013), which are

discussed in detail in later sections.

ii The statistical analysis undertaken in our 30-year review (Turner, 2008) was not reproduced here

as the changes would be minor, and add little further to the assessment.

iii Earth Trends, World Resources Institute (source: United Nations).

iv FAO Statistics, Food and Agriculture Organization, United Nations.

v UN Statistics, UNSD 2006, table 5, p. 22, UNSD 2008, table 5, p. 14.

vi UNESCO Statistics, UNESCO Institute for Statistics, 2013.

vii Trends in Atmospheric Carbon Dioxide, Earth System Research Laboratory, NOAA, and CO2 Concentration at Mauna Loa Observatory, Hawaii, Scripps CO2 Program, University of California - San Diego.

References

Alexander, S. 2014, The New Economics of Oil, MSSI Issues paper No. 2, Melbourne Sustainable Society

Institute, The University of Melbourne.

Alghalith, M. 2010,The interaction between food prices and oil prices, Energy Economics, 32,

pp.1520-1522.

Bardi U. 2011, The Limits to Growth Revisited, Springer, New York.

Castro, R. 2012, Arguments on the imminence of global collapse are premature when based on

simulation models, Gaia-Ecological Perspectives for Science and Society, 21, pp. 271-273.

Chen, S.T., Kuo, H.I. & Chen, C.C. 2010, Modeling the relationship between the oil price and global

food prices, Applied Energy, 87, pp. 2517-2525.

Dale, M., Krumdieck, S. & Bodger, P. 2011, Net energy yield from production of conventional oil,

Energy Policy, 39, pp. 7095-7102.

Das, S. 2011, Extreme Money: Masters of the Universe and the Cult of Risk, FT Press, New Jersey, US.

De Jongh, D. C. J. 1978, Structural parameter sensitivity of the limits to growth world model,

Applied Mathematical Modelling, 2, pp. 77-80.

Diamond J. 2005, Collapse: How Societies Choose to Fail or Survive, Penguin Group, UK.

Fantazzini, D., Höök, M. & Angelantoni, A. 2011, Global oil risks in the early 21st century, Energy

Policy, 39, pp. 7865-7873.

Friedrichs, J. 2010, Global energy crunch: How different parts of the world would react to a peak oil

scenario, Energy Policy, 38, pp. 4562-4569.

Gargett, D. & BITRE 2009, Transport Energy Futures: long-term oil supply trends and projections,

Canberra ACT: Bureau of Infrastructure, Transport and Regional Economics.

Greer, J. M. 2005. How Civilizations Fall: a theory of catabolic collapse, WTV.

Greer, J. M. 2008, The Long Descent: A Users Guide to the End of the Industrial Age, New Society

Publishers, Canada.

Hall, C. A. S. & Day J. W. 2009, Revisiting the Limits to Growth After Peak Oil, American Scientist, 97,

pp. 230-237.

Hamilton, J.D. 2009, Causes and Consequences of the Oil Shock of 2007-08, Brookings Papers on

Economic Activity, 1, pp. 215-83.

Harich, J. 2010, Change resistance as the crux of the environmental sustainability problem, System

Dynamics Review, 26, pp. 35-72.

Heinberg, R. 2007, Peak Everything: waking up to the century of declines, New Society Publishers,

Canada,

Heinberg, R. 2009, Searching for a miracle: Net Energy limits and the fate of industrial society, A

joint report from the International Forum on Globalization, the Post Carbon Institute, accessed:

www.postcarbon.org/new-site-files/Reports/Searching_for_a_Miracle_web10nov09.pdf

Heinberg, R. 2011, The End of Growth: adapting to our new economic reality, New Society Publishers,

Canada.

Heun, M. K. & De Wit, M. 2012, Energy return on (energy) invested (EROI), oil prices, and energy

transitions, Energy Policy, 40, pp.147-158.

Hirsch, R. L. 2008, Mitigation of maximum world oil production: shortage scenarios, Energy Policy, 36,

pp. 881-889.

Hirsch, R. L., Bezdek, R. & Wendling, R. 2005, Peaking of World Oil Production: impacts, mitigation and risk

management, National Energy Technology Laboratory (NETL), Department of Energy, West Virginia,

US

Hubbert, M. K. 1956, Nuclear Energy and the Fossil Fuels, Shell Development Company, Houston, Texas.

Hubbert, M. K. 1982, Oil and Gas Supply Modeling, U.S. Department of Commerce / National Bureau

of Standards (now the National Institute of Standards and Technology, NIST), US.

Keen, S. 2009, Bailing out the titanic with a thimble, Economic Analysis & Policy, 39, pp. 3-25.

Linner, B.O. & Selin, H. 2013, The United Nations conference on sustainable development: forty

years in the making, Environment and Planning C: Government and Policy, 31, pp. 971-987.

Lomborg, B. & Rubin, O. 2002, The dustbin of history: limits to growth, Foreign Policy, 133, pp. 42-44.

Maugeri, L. 2012, Oil: The Next Revolution, Discussion Paper 2012-10, Belfer Center for Science and

International Affairs, Harvard Kennedy School, Harvard University, US.

Meadowcroft, J. 2013, Reaching the Limits?, Environment and Planning C: Government and Policy, 31, pp.

988-1002.

Meadows, D. H., Meadows, D. L., Randers, J. & Behrens III, W. W. 1972, The Limits to Growth, Universe

Books, New York, US.

Meadows, D. L., Behrens III, W. W., Meadows, D. H., Naill, R. F., Randers, J. & Zahn, E. K. O. 1974,

Dynamics of Growth in a Finite World, Wright-Allen Press, Massachusetts, US.

Murphy, D. J. & Hall, C. A. S. 2010, Year in review-EROI or energy return on (energy) invested,

Annals of the New York Academy of Sciences, 1185, pp.102-118.

Murphy, D. J. & Hall, C. A. S. 2011, Energy return on investment, peak oil, and the end of economic

growth, Annals of the New York Academy of Sciences, 1219, pp. 52-72.

Murray, J. & King, D. 2012, Climate policy: Oils tipping point has passed, Nature, 481, pp. 433-435.

Murray, J. W. & Hansen, J. 2013, Peak oil and energy independence: myth and reality, Eos, Transactions

American Geophysical Union, 94, pp. 245-246.

Neff R. A., Parker, C. L., Kirschenmann, F. L., Tinch, J. & Lawrence, R. S. 2011, Peak oil, food systems,

and public health, American Journal of Public Health, 101, pp.1587-1597.

Nel, W. P. & Cooper, C. J. 2009, Implications of fossil fuel constraints on economic growth and global

warming, Energy Policy, 37, pp. 166-180.

Orlov, D. 2008, Reinventing Collapse, New Society Publishers, Canada.

Randers, J. 2012, 2052: A Global Forecast for the Next Forty Years, Chelsea Green Publishing, Vermont

US.

Randers, J. 2012, The real message of the Limits to Growth: a plea for forward-looking global

policy, Gaia-Ecological Perspectives for Science and Society, 21 (2), pp. 102-05.

Raskin, P. D., Electris, C. & Rosen, R. A. 2010, The century ahead: searching for sustainability,

Sustainability, 2, pp. 2626-2651.

Rickards, L., Wiseman, J. and Kashima, Y. (In press) Barriers to effective mitigation actions on climate

change: the case of senior government and business decision-makers, Wiley Interdisciplinary Review,

Climate Change.

Schwartz, B. S., Parker, C. L., Hess, J. & Frumkin, H. 2011, Public health and medicine in an age of

energy scarcity: the case of petroleum, American Journal of Public Health, 101, pp. 1560-1567.

Simmons, M.R., 2000, Revisiting the Limits to Growth: could the Club of Rome have been correct,

after all?, An Energy White Paper, accessed: www.simmonsco-intl.com/files/172.pdf.

Sorrell, S., Miller, R., Bentley, R. & Speirs, J. 2010a, Oil futures: A comparison of global supply forecasts,

Energy Policy, 38, pp. 4990-5003.

Sorrell, S., Speirs, J., Bentley, R., Brandt, A. & Miller, R. 2010b, Global oil depletion: A review of the

evidence, Energy Policy, 38, pp.5290-5295.

Tainter, J. A. 1988, The Collapse of Complex Societies, Cambridge University Press, Cambridge, UK.

Turner, G. M. 2008, A comparison of The Limits to Growth with 30 years of reality, Global Environmental

Change, 18, pp. 397-411.

Turner, G. M. 2012, On the cusp of global collapse? Updated comparison of the Limits to Growth

with historical data, GAiA - Ecological Perspectives for Science and Society, 21, pp.116-124.

Turner, G. M. 2013, The limits to growth model is more than a mathematical exercise; reaction to R.

Castro, 2012, Arguments on the imminence of global collapse are premature when based on

simulation models, GAiA 21/4, pp. 271 273. GAiA, 22, pp.18-19.

Vermeulen, P. J. & De Jongh, D. C. J. 1976, Parameter sensitivity of the Limits to Growth world

model, Applied Mathematical Modelling, 1, pp. 29-32.

Acknowledgments: This Paper draws substantially on the following publication, with additional material incorporated: Turner G 2012, On the cusp of global collapse? Updated comparison of the Limits to Growth with historical data. GAiA, 21, pp. 116-124.

Citing this report: Please cite this paper as Turner, G. (2014) Is Global Collapse Imminent?, MSSI Research Paper No. 4, Melbourne Sustainable Society Institute, The University of Melbourne.

ABOUT THE AUTHOR

Dr. Graham M. Turner is a Principal Research Fellow at the Melbourne Sustainable Society Institute (MSSI), University of Melbourne, Australia. The MSSI aims to facilitate and enable research linkages, projects and conversations leading to increased understanding of sustainability and resilience trends, challenges and solutions. The MSSI approach includes a particular emphasis on the contribution of the social sciences and humanities to understanding and addressing sustainability and resilience challenges. MSSIs Research Papers Series is a key communication initiative aimed at stimulating thought and discussion within the University of Melbourne and broader community and showcasing the scholarship of MSSI. The editor is Dr. Lauren Rickards.

|

![[groups_small]](groups_small.gif)