|

Mother Pelican

A Journal of Solidarity and Sustainability

Vol. 10, No. 8, August 2014

Luis T. Gutiérrez, Editor

|

|

|

|

|

|

|

Picketty Acknowledges a Limit to Inequality

Will He Acknowledge the Limits to Growth?

James Magnus-Johnston

This article was originally published in

The Daly News, 17 July 2014

under a Creative Commons License

The Center for the Advancement of the Steady State Economy (CASSE) is a research group on economic sustainability located in Arlington, Virginia, USA. The mission of CASSE is "to advance the steady state economy, with stabilized population and consumption, as a policy goal with widespread public support."

|

|

In Pickettys celebrated new work, Capital in the 21st Century, we are treated to a robust argument about the mechanics of worsening structural inequality. He narrates why owners of capital assetsstocks, bonds, and real estatehistorically realize higher returns than wage workers. Picketty uses econ-speak to describe this as a gap in the capital-income ratio, and explains how our present system is engineered to favour capital-owners or rentiers. In the 21st century, he predicts slower growth in population and productivity, but a higher rate of return on capital, pushing us into inequality levels not seen since the 19th century.

But the limits we face are far greater than limits to just the capital-income ratio. While many of us share Pickettys anxiety about worsening inequality (for me, every time I see a headline celebrating the rise of house prices), worsening structural inequality at this stage in history is but one symptom of our obsession with growth. Like Picketty, many post-growth thinkers are calling for a system change so the distribution of wealth will not inevitably concentrate in fewer and fewer hands. But rather than Pickettys proposed progressive tax on wealth, we are calling for a fundamental adjustment to the financial system to make it more socially equitable and ecologically sustainable.

It might be helpful to interrogate the question of inequality this way:

- Why is it that rentiers can achieve such high rates of net worth?

Because overly-inflated asset values make rentiers look great on paper, and those funds can be leveraged for even more consumption.

- How did asset values become so inflated in the first place?

Because everyone from hedge fund managers to real estate investors bid up prices.

- Why can prices be bid up?

Because banks lend out historically unprecedented amounts of money in the form of debt.

- Why do we need so much debt?

Because if we fail to grow by at least the rate of interest, the entire financial system enters a state of default and collapse! Herman Daly proposes an increase to the fractional reserve requirement so that banks are able to lend out real money instead of just creating more debt.

While Picketty does acknowledge how the financialization of the economy in no way contributes to the real economy, he stops short of acknowledging that the volume of debt-money in the economy makes money scarce for some and abundant for others, and that the system is set up to either grow exponentially or fail spectacularly. More dubiously, in Robert Solows review of Pickettys book, Solow suggests that a society or the individuals in it can decide to save and to invest so much that they (and the law of diminishing returns) drive the rate of return below the long-term growth rate. Not so in a debt-backed monetary system steeped in stratospheric and unprecedented levels of debt!

Picketty similarly avoids acknowledging peak oil or limits to energy returns. At the most fundamental level, economic growth and capital accumulation require huge flows of matter and energy. This important consideration takes the form of but a few small caveats in Pickettys book. He predicts that wealthy countries will grow at a rate of 1.2 percent, while acknowledging that such a growth rate can only be achieved as new sources of energy are developed to replace hydrocarbons. Im not sure how this prediction can be taken seriously when we are always and everywhere these days confronted by diminishing energy returns. These limits are evident in our reliance on unconventional oil, including fracking, the tar sands, and all of the new hazards that come with shipping it, such as building new pipelines and ports in fragile ecological zones, the release of methane and other undesirables from fracking, and the looming spectre of another Lac Megantic disaster. Add to this the uncounted costs of climate changefrom private insured losses to government disaster expensesand we wind up in the highly questionable position of counting disaster rebuilding efforts as additions to GDP!

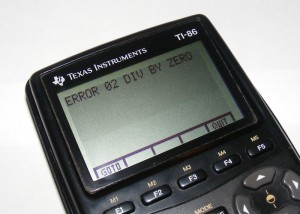

What happens if Picketty assumes a growth rate of zero? ERROR.

|

Perhaps, interpreted liberally, Pickettys prediction of 1.2 percent growth is a couched acknowledgement that we have a failed growth economy on our hands. Or perhaps there is an even simpler methodological explanation for Pickettys prediction, which is that if he were to assume a growth rate of zero, the law he appliesbeta equals savings divided by growthwould yield absolutely no results whatsoever! And who can make newsworthy predictions with a divide-by-zero error message?

Pickettys research is certainly useful and clearly resonates with a disillusioned public seeking to understand the causes of growing inequality. But without full acknowledgement of the limits to growth, there are also limits to his historical analogiesafter all, the extent of ecological overshoot makes this period remarkably different from any period before it. Which means that the laws and formulae used throughout his book must be taken with a healthy dose of skepticism. EF Schumacher wrote

economists themselves, like most specialists, normally suffer from a kind of metaphysical blindness, assuming that theirs is a science of absolute and invariable truths, without any presuppositions. Some go as far as to claim that economic laws are as free from metaphysics or values as the law of gravitations.

Picketty makes a compelling, historically grounded argument about worsening structural inequality. But perhaps we can call for bolder action to respond to contemporary problems, including serious financial reform that reduces or extinguishes unsustainable debt; nurturing a grassroots movement toward more equitable, democratic work structures (so that more people have access to assets and ownership in the first place); and teaching a new generation of economists that all financial capital is fundamentally a gift from nature.

|

ABOUT THE AUTHOR

James Magnus-Johnston has worked in the financial industry, in policy positions with lawmakers, and in the communications industry as an editor. He has an MPhil in Economics from Cambridge University, where he completed a thesis on the growth dynamics imposed by the global banking system. He is presently a professor of Political Studies and Economics with Canadian Mennonite University, the social enterprise development liaison with Manitobas Green Action Centre, and a member of Transition Winnipegs Initiating Committee. In his work, James promotes the transition to a steady state economy through financial reform, low-impact living, and the use of entrepreneurship to ignite change. Contact James via email.

ABOUT THE CENTER FOR THE ADVANCEMENT OF THE STEADY STATE ECONOMY

The Center for the Advancement of the Steady State Economy (CASSE) is a research group on economic sustainability located in Arlington, Virginia, USA. The mission of CASSE is "to advance the steady state economy, with stabilized population and consumption, as a policy goal with widespread public support." The CASSE website provides many additional research resources on economic growth, degrowth, and post-growth. For example:

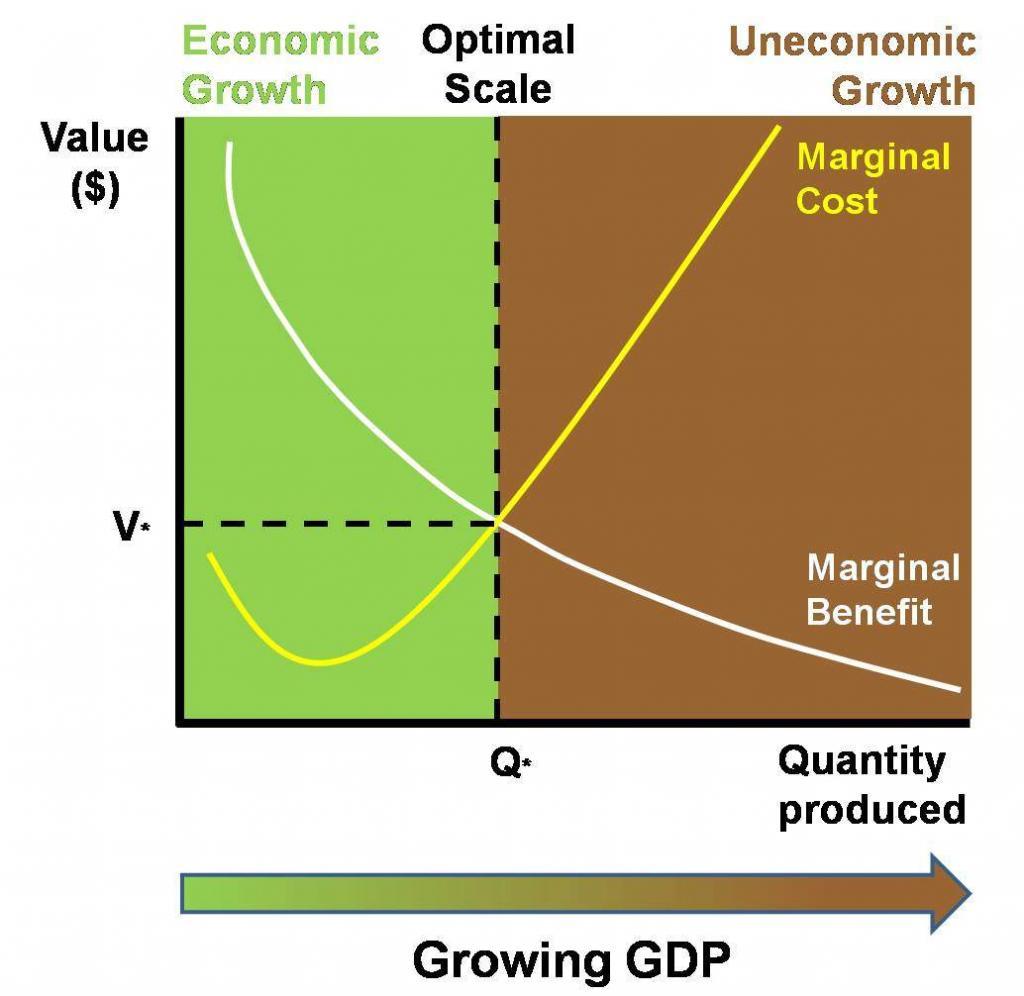

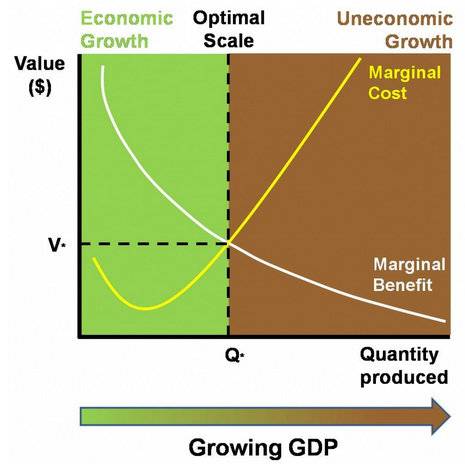

The following chart captures the basic rationales for the steady-state economy:

"Marginal cost refers to the cost of producing one more unit of a good or service. Marginal benefit is the benefit gained from one more unit. This graph shows the marginal costs and benefits of GDP growth. Costs tend to rise and benefits tend to decrease for each additional unit of growth. We should stop growing GDP, therefore, when marginal costs are exactly equal to marginal benefits. If costs are less than benefits, then GDP growth is economic (the green part of the graph). When costs rise above benefits, GDP growth is uneconomic (the brown part)."

|

Additional articles on the application of the fundamental steady-state economy concept to specifc issues can be found in the

The Daly News. The following is a list of recently published articles:

Steady Statesmanship Goes Global,

by Jon Rosales, The Daly News, 17 June 2013

Full Employment Versus Jobless Growth, Herman Daly, The Daly News, 15 July 2013

Entropia: Life Beyond Industrial Civilisation,

Samuel Alexander, The Daly News, 1 August 2013

Fixing Food and Farming with a True-Cost Economy, Brent Blackwelder, The Daly News, 6 August 2013

The End of the Age of Extraction, Brent Blackwelder, The Daly News, 2 September 2013.

Approaching a Steady State Economy, Part 1 Getting Around, Rob Dietz, The Daly News, 9 September 2013

Approaching a Steady State Economy, Part 2 Clean Clothes, Rob Dietz, The Daly News, 16 September 2013

Growth and Laissez-faire, Herman Daly, The Daly News, 23 September 2013.

Unlimited Competition Is Not Sustainable, Gunnar Rundgren, The Daly News, 30 September 2013.

Insanity Reigns at the World Bank, Brent Blackwelder, The Daly News, 14 October 2013.

A Question of Scarcity, Andrew Fanning, The Daly News, 21 October 2013.

How Many People Can a State Sustain?, George Plumb, The Daly News, 4 November 2013.

The Five Dumbest Things Youll Hear About Sustainability, Brian Czech, The Daly News, 12 November 2013.

Top 5 Threats to the Worlds Beaches (and a Systemic Solution), Brent Blackwelder, The Daly News, 18 November 2013.

The Hidden Door: Mindful Sufficiency as an Alternative to Extinction, Mark Burch, The Daly News, 16 December 2013.

Voluntary Simplicity and the Steady-State Economy, Mark Burch, The Daly News, 7 January 2014.

Toward a Finite-Planet Journalism, Eric Zencey, The Daly News, 3 February 2014.

Who's Going to Lead the Way to a Sustainable Economy?, by Rob Dietz, The Daly News, 24 February 2014.

An Economic Game Plan to Prevent Water Pollution, Brent Blackwelder, The Daly News, 17 March 2014.

What to Do When You Suspect Were Headed for Collapse, Rob Dietz, The Daly News, 31 March 2014.

GDP: The Infinite Planet Indicator, Eric Zencey, The Daly News, 30 May 2014.

Fresh Water, Growth, Degrowth, and the Steady State Economy, Geoffrey Matthews, The Daly News, 12 June 2014.

Gross Domestic Problem: Dont Shoot the Measurement, Brian Czech, The Daly News, 3 July 2014.

Cold War Left Overs, Herman Daly, The Daly News, 29 July 2014.

|

|Back to TITLE|

Page 1

Page 2

Page 3

Page 4

Page 5

Page 6

Page 7

Page 8

Page 9

Supplement 1

Supplement 2

Supplement 3

Supplement 4

Supplement 5

Supplement 6

PelicanWeb Home Page

|

|

|

|

"Patriarchy dehumanizes both women and men."

Leonardo Boff, Brazil, 2014

|

|

Page 3

|

|

FREE SUBSCRIPTION

|

![[groups_small]](groups_small.gif)

|

Subscribe to the

Mother Pelican Journal

via the Solidarity-Sustainability Group

Enter your email address:

|

|

|

|