|

'The longer we wait, the costlier it will be': IPCC's latest climate assessment makes it perfectly clear that solutions to crisis exist, but political atrophy spells doom.

The latest report by the Intergovernmental Panel on Climate Change (IPCC), released Sunday in Berlin, shows that humanity still has time to solve the global crisis of global warming and climate change, but only if governments and industry are finally forced to make the political and financial decisions that will see the rapid reduction of CO2 emissions while launching a planetary push for renewable energy sources. Environmentalists responded to the report by saying that its findings simply go to show that far from showing a 'green energy revolution' is expensive or prohibitive, the opposite is true.

"Dirty energy industries are sure to put up a fight but it's only a question of time before public pressure and economics dictate that they either change or go out of business. The 21st century will be the 'age of renewables'." Kaisa Kosone, Greenpeace

|

"Clean energy is not costly, but inaction is," said Greenpeace campaigners Daniel Mittler and Kaisa Kosonen from Berlin. "Costly in terms of lives, livelihoods and economies if governments and business continue to allow climate change impacts to escalate."

According to the Working Group III contribution to the IPCCs Fifth Assessment Report, it remains possible, "using a wide array of technological measures and changes in behaviour," to limit the increase in global mean temperature to two degrees Celsius above pre-industrial levels as world governments have agreed is the target for this century. However, says the report, only "major institutional and technological changes" will do and they must be done immediately without the delays and obstructions that have so far blocked meaningful action.

The key message of the report is that the burning of fossil fuels must be rapidly curbed and phased out, while the investments in renewable, low- or zero-carbon sources of energy must be scaled up dramatically. And, as Mittler and Kosonen summarize, the economic, ecological, and societal realities prove that "climate action is an opportunity, not a burden."

The longer we wait, the costlier it will be, said Charles Kolstad, an environmental economist at the University of California, Santa Barbara, and the report's lead author.

Climate policies in line with the two degrees Celsius goal need to aim for substantial emission reductions, said Ottmar Edenhofer, one of the co-chairs of the report. There is a clear message from science: To avoid dangerous interference with the climate system, we need to move away from business as usual.

The report, entitled Climate Change 2014: Mitigation of Climate Change, is the third of three Working Group reports, which, along with a Synthesis Report due in October 2014, constitute the IPCCs Fifth Assessment Report on climate change.

"The solutions to make the shift from fossil fuels to renewables are clear," says Hoda Baraka, global communications manager for the climate action group 350.org. "We need to stop pumping money into a rogue industry that is determined to maximize its profits at any cost. Divestment is the means to shift investments away from coal, oil and gas companies and into a more equitable and sustainable energy economy."

As Greenpeace's Kosonen said in a statement: "Renewable energy is unstoppable. It's becoming bigger, better and cheaper every day. Dirty energy industries are sure to put up a fight but it's only a question of time before public pressure and economics dictate that they either change or go out of business. The 21st century will be the 'age of renewables'."

Reporting on the IPCC's findings, the Guardian's Damian Carrington notes that solving the crisis is 'eminently affordable' compared to the disaster of doing nothing. Focusing on the various mitigation options included in the report, he writes:

Along with measures that cut energy waste, renewable energy such as wind, hydropower and solar is viewed most favourably by the report as a result of its falling costs and large-scale deployment in recent years.

The report includes nuclear power as a mature low-carbon option, but cautions that it has declined globally since 1993 and faces safety, financial and waste-management concerns. Carbon capture and storage (CCS) trapping the CO2 from coal or gas burning and then burying it is also included, but the report notes it is an untested technology on a large scale and may be expensive.

Biofuels, used in cars or power stations, could play a critical role in cutting emissions, the IPCC found, but it said the negative effects of some biofuels on food prices and wildlife remained unresolved.

The report found that current emission-cutting pledges by the worlds nations make it more likely than not that the 2C limit will be broken and it warns that delaying action any further will increase the costs.

Friends of the Earth energy program director Ben Schreiber said the IPCC has done its job and now it is time for governments to finally stand up and do theirs.

"Time is running out," said Schreiber, "but we can still alter our current trajectory before it leads to climate disaster. Unfortunately, even as the worlds leading scientists are laying out the need for urgent action, the political leaders at the negotiating table remain unwilling to commit to the steps necessary."

Schreiber pointed the finger at the United States, the largest historic emitter of greenhouse gasses, and said the all of the above energy policy of President Obama is incompatible with "the overwhelming evidence that we must leave fossil fuels in the ground." Coal and natural gas, he said, have no place in our climate constrained world and the White House and other leading developed nations must finally face their special responsibility to lead, not obstruct, the path towards a new energy paradigm.

Analysts at the Energy Desk compiled the report's 15 key findings here.

And IPCC Chairman, Rajendra Pachauri, released this video to state the importance of the IPCC's work overall and the significance of its latest report:

Source: IPCC Assessment Report, 11 April 2014

Jon Queally is a senior editor and staff writer with Common Dreams. He has been with Common Dreams since 2007 covering US politics, foreign policy, human and animal rights, climate change, and much in between. In addition to his role as the opinion editor, he works daily on the creation, selection and management of news content. Email: jon@commondreams.org.

|

Limits to Investment: Finance in the Anthropocene

John Fullerton

This article was originally published in

Great Transition Initiative, April 2014

under a Creative Commons License

"The true nature of the international system under which we were living was not realized until it failed." ~ Karl Polanyi

|

A transition to a sustainable economy requires not only population stabilization, breakthroughs in resource productivity, and checks on material consumption, but also constraints on aggregate investment. Built into the DNA of finance is the goal of optimizing relatively short-term returns on investment, which, when successful, induces exponential growth in the aggregate stock of financial capital. When that expanding stock of financial capital is then reinvested, it spurs ever-increasing demands for natural resources and pressure on waste sinks. The contradiction between the finite scale of the biosphere and the endless growth of finance capital will be resolved either through crisis or, as advocated here, through foresight and remedial action. Shifting the economic system demands a fundamental transformation of finance, at least for the real investment decisions of the largest actors in the economy. We must view this profound shift as a critical national and global security priority that will require unprecedented intervention by governing institutions on the publics behalf.

Context | The Impact of Investment | From the Firm to the System |

The Way Forward | Endnotes

Context

The egregious offenses of modern finance need little elaboration. The finance-induced Great Recessionstill a depression in parts of the European Unionhas been causing oppressive pain and suffering, with multi-generational consequences, including increased wealth inequality, cascading throughout the global economy. If we can peer beyond the human wreckage, we may glimpse a silver lining: the lingering economic crisis has provided even mainstream economists a reason to question as never before the very foundations of our finance-driven economic system. Just as dangerous as rogue banks too big to fail or to governand the predatory casino finance that has become their stock-in-tradeis the growth imperative that drives the modern economy beyond the resource and waste sink limits of the biosphere.

Finances most important practical functions in the real economy are the transformation of savings into investment and the credit creation process of the banking system. The reorientation of the flow of real investment (not to be confused with financial asset speculation) is the bridge to, and the steering mechanism for, a Great Transition to an economy that serves people while respecting the ecospheres physical limits. For now though, the same planetary boundaries that dictate limits to growth also imply limits to investment, since investment fuels growth. No economic system in the history of civilization has ever had to contemplate such a constraint. How much and where large economic actors like multinational corporations and nation-states invest will significantly determine the quality of the economic system of the future and, given present social and ecological stresses, our collective well-being and global security. As a consequence, real investment choices must become a central concern of global governance, notwithstanding the many failings of governing institutions.

The Impact of Investment

The economy, as measured by Gross National Product (GNP), includes consumption, investment, government spending, and net exports, often rendered as a simple equation:

GNP = C + I + G + netX

Concern for sustainability has typically focused on consumption since it represents the largest share of the economy (70 percent in the US, less in emerging economies like China and India). However, capital investment has a disproportionately large impact because of the long-term implications it has on future consumption through technology lock-in and the embedded feedback loops of business enterprise. For example, if an automobile company constructs a factory to build SUVs, then its advertising and sales efforts will focus on increasing the demand for these SUVs.

Distinguishing between financial investment and real investment is critically important. The former has attracted considerable attention in the investment community: witness the debates about the impact of SRI (socially responsible investment) and related ESG factors (environmental, social, and governance) on corporate behavior and investment performance. Yet financial investors and speculatorsgroups that increasingly blur togetherare typically far removed from the real capital investment decisions of the large public corporations that, to a significant extent, drive and shape the material economy. Even some leading practitioners of ESG and sustainable investment acknowledge that ESG is primarily a risk mitigation strategy for financial investment portfolios, rather than a transformational strategy for the real economy.1

The top 1,000 global corporations represent half of the total market value of the worlds 60,000 public companies and, undoubtedly, an even greater share of capital investment budgets.2 What demands our attention, therefore, are the decades-long impacts of the capital expenditure decisions of these largest corporations, together with the impacts of large government capital expenditures like investments in infrastructure. Corporate reporting on social and environmental performance, however, tends to focus on supply chain impacts rather than the initiating impact of the capital expenditures that create these supply chains. To take one of the worlds largest corporations as an example, Walmarts continued investment in new superstores matters much more than its subsequent efforts to green its supply chain, notwithstanding the importance of that work.

Shareholder engagement that focuses on capital investment decisions will inevitably confront pushback rooted in concerns about long-term growth, competitiveness, and share price. Corporations make their investment decisions using an internal rate of return framework that compares a projects expected financial return with the firms cost of capital. Because of the way finance discounts the future, corporations approve capital expenditures that achieve financial return targets with time horizons that rarely exceed ten years and typically ignore externalities, including those with serious long-term risks. Concerns about the systemic impact on social and natural capital rarely enter the analysis. They are managed afterward, if at all. This short-termism is compounded by the even shorter-term horizon of financial investors and speculators preoccupied with quarterly earnings and higher valuations in the stock market.

Policy responses, moreover, rarely occur until after enterprise investment decisions have already been made. A company is free to build a cigarette industry, and only afterwards does society respond with labeling and advertising policies that, at best, partially mitigate the damage. Today, unprecedented ecological risks make this reactive approach unacceptable. Many forward-thinking CEOs and policymakers fully understand this new reality yet feel powerless to change it.

From the Firm to the System

An adequate response to the challenge of a world at risk requires turning from the firm-level investment decisions to the economic system as a whole.3 Along with genuine contributions to human progress, our economic system has produced staggering growth in financial wealth. Financial assets in the US have doubled as a percentage of GDP since 1980.4 This should give us pause, rather than reason for celebration.

The drive for exponential returns on financial capital pushed finance to shorter-term and more speculative activity at the same time as physical resource limits to growth began to impose constraints. This has come at an alarming cost. Of the twenty largest countries in the world, constituting nearly three-quarters of global GDP, all but Japan suffered per capita losses in their natural capital stocks between 1990 and 2008.5 Although natural capital can be eroded for decades, we already appear to have passed safe limits, most notably the atmospheres limit to absorb carbon waste.6

In the full world context in which we now find ourselves, quantitative limits to aggregate material growth logically imply limits to investment. Our challenge is now to determine where we invest and what we grow. Energy and material efficiency in the industrialized world and investments in support of healthy lives with dignity for the less developed economies are obvious top priorities.7 Investments in fossil fuel-hogging luxury yachts and indoor skiing in the Dubai desert are not.

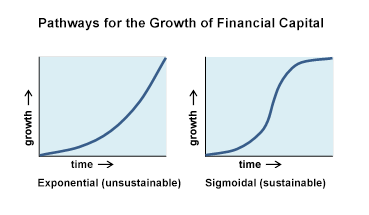

Continuing the pursuit of exponential growth of financial capital by drawing down both social and natural capital is unsustainable. Simple arithmetic demands that it will eventually generate some combination of financial, social, or ecological collapse. With the Great Recession as a wake-up call, we can begin to seek ways to shift the growth trajectory of financial capital from an exponential curve to a more sustainable (sigmoidal) growth curve as found in natural systems.

Thriving individual enterprisesparticularly the ones needed to drive the economic transitioncan and will continue to grow and deliver exponential returns to investors, at least for a while. However, even accounting for unanticipated efficiency gains in the energy and material intensity of the economy, the aggregate stock of financial capital will need to pass through a critical inflection point to declining rates of growth.8 This transition can occur through some combination of the following developments, many of which are already underway:

- a declining aggregate rate of return on invested capital,

- a systematic financial asset devaluation,

- the debasing of currencies through inflation,

- defaults leading to voluntary or involuntary debt extinguishment,

- an unprecedented scale of private philanthropy to recycle financial capital back into social and natural capital,

- a large-scale voluntary or policy-induced reinvestment of profits by the corporate sector into natural and social capital, and

- an increase in taxation to allow the public sector to recycle financial capital back into natural and social capital on behalf of vital public security interests.

We can choose to lead this transition to reduced growth in the stock of financial capital, while augmenting the stocks of social and natural capital, or risk having it forced upon us by natures limits, social upheaval, ormost likelyboth at the same time.

The Way Forward

The scale and complexity of the required shift in understanding is unparalleled, and time is not on our side. Not only are we in ecological overshoot, drawing down our life-sustaining stock of natural capital and putting social cohesion at risk because of growing inequality and related social stresses, but we are no doubt in financial overshoot as well.9 Financial overshoot exists to the extent that financial assetsboth stocks and bondsare valued by a marketplace that has not yet fully accounted for the multi-decade adjustment process ahead in which honest pricing of externalities and the real resource constraints of planetary boundaries constrain aggregate growth rates. If this transition is left unmanaged, the feedback loops of financial asset valuation adjustments into the real economy could unleash chaos as we now know all too well.

Three interconnected solutions are apparent, all immensely challenging. First, we can work within the current neoliberal economic paradigm to shift the flow of investment by internalizing the costs of the externalities that we currently ignore. Second, business, government, and large pools of private capital can begin leading through enlightened real investment and integrated philanthropy even before a world of accurate accounting using honest pricing is realized. Third, the public can demand a new set of rules and regulationssome local, some regional, some globalto establish the necessary guardrails and mandates for the transition.

Getting prices right: Commercial enterprises must begin to pay the true social and environmental cost of their operations. Establishing sound measurement procedures and mandatory transparency is an essential first step, and many integrated reporting initiatives show promise despite difficulties in enforcement.10 Critically, however, the presumption that we can put a correct price on many of these costs is naïve and dangerous. Some costs represent harms that can be mitigated, while others represent wrongs that never can. The value of a life in a life insurance policy is certainly not the true value of that life. This same principle applies to the value of healthy ecosystem functioningnot a life, but lifewhich is literally priceless. Getting prices right to the extent possible is a necessary, but insufficient, response.

Enlightened private behavior: Progress is underway as smart companies and communities are investing in resource productivity and alternative energy to save money and accelerate the shift to a regenerative economy. Experimentation with forms of enterprise that better align all stakeholder interests, from partnerships and cooperatives to for-benefit corporations (B-Corps) and innovative forms of social enterprise, is accelerating.11 A small group of entrepreneurs and enlightened stewards of capital are leading the way, albeit at a pace too slow and a scale too small. Could a group of large actors including businesses, governments, sovereign wealth funds, pension funds, foundations and endowments, and high net worth familiesunshackled from speculative capital markets no longer fit for purpose and using innovative investment methodswork collectively to alter the course and quality of the economy through their aggregate real investment decisions and approaches?12 Or will the emergent bottom-up, distributed innovation fueled by crowdsourcing scale to such a degree that it impacts the global economic system?

The answer remains unclear. On the one hand, climate stabilization demands that we not burn the vast majority of known fossil fuel reserves already sitting on company balance sheets, yet the energy industry continues to invest hundreds of billions of dollars per year in search of more.13 On the other hand, real progress is afoot within the most progressive corporations, without which meaningful and peaceful economic transition would be difficult, if not impossible. A growing community of wealthy families, foundations, and sovereign wealth funds are engaging in impact investing and philanthropy to harmonize ecological and social impact with financial returns. But the critical large-scale expansion of this integrated approach, particularly the recycling of financial capital back into natural capital, has yet to emerge.

Public policy responses: No realistic assessment of the transition ahead, even by the most steadfast advocates of technology-driven and market-based solutions, can fail to see the primacy of the public sectors role in catalyzing this unprecedented shift. We will need new regulatory frameworks and incentives to help steer an economic transition more profound than the Industrial Revolution. Economically obvious but politically difficult policies like carbon caps and/or taxes must contribute to a portfolio of tools for curbing greenhouse gas emissions along with expanded research and development in clean technology. Action to remove subsidies from fossil fuel-based energy and agriculture and shift them to drive improved resource productivity and accelerated growth of renewable energy and sustainable agriculture is long overdue.

However, a larger and more uncomfortable requirement looms. In the full world of the Anthropocene, our notions of freedom will need to adjust to new realities.14 Simply encouraging so-called green investment will not be enough if we do not curtail investment that has negative and even catastrophic impacts. Deciding the qualitative what and the absolute scale of investment must become a matter of the public interest. Logic then points to a fresh and expanded need for governance, even though our confidence in government at the moment is low (or nonexistent) because of valid concerns about competence and corruption. New and effective approaches to global and regional governance, likely using cities as the central nodes of coordinating power, are essential.

In the crises ahead, the impossible will become the inevitable. The belief in the unencumbered freedom of large corporations and other large economic actors to make investment decisions that may have catastrophic and irreversible consequences must now be challenged. Activists fighting deforestation in the Amazon and the construction of the Keystone XL pipeline are showing the way forward. We must begin to accept some form of public interest influence over both the scale and direction of private and public investment capital flows as vital to our national and global security interests.

Opponents will inevitably attack this idea as socialism or worse. But it addresses a profoundly different issue than concerns about the ownership of the means of production. Given the linkage between investment and material throughput of the economy, how we choose to invest will determine to a significant degree whether we follow a path to a Great Transition or continue on the present course to societal destabilization and environmental collapse.

We can look to the public utility sectors (imperfect) permitting process for precedents of regulatory engagement in capital investment decisions at regional scale.15 Numerous state and multilateral actors, such as the World Bank, already influence the course of investment capital flows globally, although not always in a positive direction. The idea is not new, but the potential scale and scope are, particularly in regard to the need to constrain certain investments like the unrestrained extraction of coal.

Central banks are obvious candidates for radical institutional reform to encompass this new imperative. Central banking in the Anthropocene might well entail qualitative mandates regarding investment and credit flows in addition to conventional inflation and full employment mandates. We must also tackle thorny questions regarding the public and private nature of banking institutions, the credit creation function which the banks now manage under a fractional reserve system, and the alignment of the mission of banks with public purpose rather than private speculation at public expense.

We will achieve our greatest impacts if we can rein in and influence the capital investment decisions of the largest corporations and the G-20 governments, as well as the credit decisions of the fifty largest global banks and financial intermediaries. Supporting public policies can achieve this while allowing more decentralized entrepreneurial energies to flourish at appropriate scale within a new macro framework. If mega-firms in the private sector fail to act in accordance with this overriding public interest, or prove to be ungovernable, we may have no alternative but to nationalize and manage them in the public interest, as Milton Friedmans revered teacher H.C. Simmons well understood in his own context.16 Although such a suggestion is fraught with huge challenges, we must look head-on at the scale and scope of the transformation we need, particularly in the fossil fuel, agriculture, and banking industries.

Can such unprecedented global oversight, even if limited to the most critical economic actors, be practical without harming the global economy? We have no choice but to try, for business-as-usual will lead to ecological and social collapseand, of course, the collapse of the economy as well. There will inevitably be short-term efficiency and growth trade-offs in exchange for system resilience. The rich countries will need to find prosperity without growth in material resource throughputin fact, with an immense increase in material efficiency.17 At the same time, the developing world will need to foster human and ecological well-being through more intelligent technology choices than currently deployed in the North.

The careful, holistic management and monitoring of aggregate real investment flows are an inevitable part of the economy of the future and the challenging transition to it. This will require new global oversight mechanisms, informed by the best scientific understanding of critical ecosystems and empowered by sovereign nation-states and global corporations, to define and enforce a safe operating space within which our innovation-driven, free-market system can thrive.18 Like the canvas for a painter, boundaries will provide the discipline that enhances creativity. The extreme degree of financial speculation that defines the financial landscape today has no place in such a future and must be curbed immediately.

Large-scale investment decisions simply must be considered a vital part of the public interest. The sooner we acknowledge the implications of this immense challenge the better.

Endnotes

1. Private communications.

2. Robert G. Eccles and George Serafeim, Top 1,000 Companies Wield Power Reserved for Nations, Bloomberg, September 11, 2012, http://www.bloomberg.com/news/2012-09-11/top-1-000-companies-wield-power-reserved-for-nations.html.

3. Although the focus here is on large firms, nurturing decentralized, low-capital enterprises will be vital to building a sustainable economy.

4. Charles Roxburgh, et al. Global Capital Markets: Entering a new era. (New York: McKinsey Global Institute, 2009), http://www.mckinsey.com/insights/global_capital_markets/global_capital_markets_entering_a_new_era.

5. International Human Dimensions Programme on Global Environmental Change, Inclusive Wealth Report: Measuring Progress Toward Sustainability (Cambridge, UK: Cambridge University Press, 2012).

6. Johan Rockstrom, A Safe Operating Space for Humanity, Nature 461 (Sept 2009): 472-475; World Footprint: Do We Fit on the Planet? Global Footprint Network, last modified June 17, 2013, http://www.footprintnetwork.org/en/index.php/GFN/page/world_footprint.

7. Hunter Lovins and Boyd Cohen, The Way Out: Kick-starting Capitalism to Save our Economic Ass (New York: Hill and Wang, 2012).

8. Of course, the abstract sigmoidal curve leaves key questions unansweredwhat grows, what shrinks, what impact will technology have, who decides, how do we manage the adjustment, and so on.

9. John Fullerton, Financial Overshoot, The Future of Finance (blog), Capital Institute, July 23, 2012, http://www.capitalinstitute.org/blog/financial-overshoot.

10. International Integrated Reporting Council, Consultation Draft of the International Framework (London: IIRC, 2013), http://www.theiirc.org/wp-content/uploads/Consultation-Draft/Consultation-Draft-of-the-InternationalIRFramework.pdf; SASB Principles, Sustainability Accounting Standards Board, last modified 2013, http://www.sasb.org/approach/principles.

11. Marjorie Kelly, Owning Our Future: The Emerging Ownership Revolution (San Francisco: Berrett-Koehler, 2012).

12. Regarding examples of such innovative investment methods, see the following: John Fullerton, Evergreen Direct Investing: A Two-Part Series, The Future of Finance (blog), Capital Institute, December 5, 2013, http://www.capitalinstitute.org/blog/evergreen-direct-investing-two-part-series#.UrYj3WRDuF5. The two-part series first appeared in CSR Wire: Evergreen Direct Investing: ESG 2.0? CSR Wire, November 19, 2013, http://www.csrwire.com/blog/posts/1111-evergreen-direct-investing-esg-2-0, and Evergreen Direct Investing: The CEO Perspective, CSR Wire, December 5, 2013, http://www.csrwire.com/blog/posts/1133-evergreen-direct-investing-the-ceo-perspective.

13. Bill McKibben, Global Warmings Terrifying New Math, Rolling Stone, July 19, 2012, http://www.rollingstone.com/politics/news/global-warmings-terrifying-new-math-20120719; John Fullerton, Big Choice, The Future of Finance (blog), Capital Institute, July 19, 2011, http://www.capitalinstitute.org/blog/big-choice-0.

14. John Fullerton, Freedom in the Anthropocene, The Future of Finance (blog), Capital Institute, June 4, 2012, http://www.capitalinstitute.org/blog/freedom-anthropocene.

15. Richard Rosen, How Should the Economy Be Regulated? (paper presented at the Second Summit on the Future of the Corporation, Corporation 20/20, Boston, MA, June 2009), http://www.corporation2020.org/corporation2020/documents/Papers/2nd-Summit-Paper-Series.pdf.

16. H. C. Simons, Economic Policy for a Free Society (Chicago: University of Chicago Press, 1948). The author is grateful to Gar Alperovitz for drawing attention to Simons views on nationalization in his New York Times op-ed: Gar Alperovitz, Wall Street Is Too Big to Regulate, New York Times, July 22, 2012, available at http://www.nytimes.com/2012/07/23/opinion/banks-that-are-too-big-to-regulate-should-be-nationalized.html.

17. Tim Jackson, Prosperity without Growth: Economics for a Finite Planet (New York: Earthscan, 2009).

18. Peter Brown and Geoffrey Garver, Right Relationship, Building a Whole Earth Economy (San Francisco: Berrett-Koehler, 2009).

John Fullerton is the Founder and President of the Capital Institute, a recognized new economy thought leader, and an active Impact private investor. He is a co-founder and director of Grasslands, LLC, a holistic ranch management company with the Savory Institute; a director of New Day Farms, Inc., the New Economics Institute, and Savory Institute.org; and an advisor to RSF Social Finance, Richard Bransons Business Leaders Initiative (B Team), and Armonia, LLC.

|

|

![[groups_small]](groups_small.gif)