|

Mother Pelican

A Journal of Solidarity and Sustainability

Vol. 10, No. 2, February 2014

Luis T. Gutiérrez, Editor

|

|

|

|

|

|

|

The Negative Natural Interest Rate and Uneconomic Growth

Herman Daly

This article was originally published in

The Daly News, 13 January 2014

under a Creative Commons License

|

In a recent speech to the International Monetary Fund economist Larry Summers argued that since near zero interest rates have not stimulated GDP growth sufficiently to reach full employment, we probably need a negative interest rate. By this he means a negative monetary rate set by the Fed to equal the natural rate, which he believes is now negative. The natural rate, as Summers uses the term, means the rate that would equalize planned saving with planned investment, and thereby, as Keynes taught us, result in full employment. With near zero monetary rates, current inflation already pushes us to a negative real rate of interest, but that is still insufficiently negative, in Summers view, to equalize planned investment with planned saving and thereby stimulate GDP growth sufficient for full employment. A negative interest rate is a stunning proposal, and it takes some effort to work out its implications.

Suppose for a moment that GDP growth, economic growth as we gratuitously call it, entails uneconomic growth by a more comprehensive measure of costs and benefits that GDP growth has now begun to increase counted plus uncounted costs by more than counted plus uncounted benefits, making us inclusively and collectively poorer, not richer. If that is the case, and there are good reasons to believe that it is, would it not then be reasonable to expect, along with Summers, that the natural rate of interest is negative, and that maybe the monetary rate should be too? This is hard to imagine, but it means that savers would have to pay investors (and banks) to use the funds that they have saved, rather than investors and banks paying savers for the use of their money. To keep the GDP growing sufficiently to avoid unemployment we would need a growing monetary circular flow, which would require more investment, which, in turn, would only be forthcoming if the monetary interest rate were negative (i.e., if you lost less by investing your money than by holding it). A negative interest rate makes sense if the goal is to keep on increasing GDP even after it has begun to make us poorer at the margin that is after growth has already pushed us beyond the optimal scale of the macro-economy relative to the containing ecosphere, and thereby become uneconomic.

A negative monetary interest rate means that citizens will spend rather than save, so savings will not be available to finance the investments that produce the GDP growth needed for full employment. The new money for investment comes from the Fed. Quantitative easing (money printing) is the source of the new money. The faith is that an ever-expanding monetary circulation will pull the real economy along behind it, providing growth in real income and jobs as previously idle resources are employed. But the resulting GDP growth is now uneconomic because in the full world the idle resources are not really idle they are providing vital ecosystem services. Redeploying these resources to GDP growth has environmental and social opportunity costs that are greater than production benefits. Although hyper-Keynesian macroeconomists do not believe this, the micro actors in the real economy experience the constraints of the full world, and consequently find it difficult to follow the unlimited growth recipe.

Summers (along with other mainstream growth economists), does not accept the concept of optimal scale of the macro-economy, nor the possibility of uneconomic growth in the sense that growth in resource throughput could reduce net wealth and wellbeing. Nevertheless, it is at least consistent with his view that the natural rate of interest is negative.

A positive interest rate restricts the total volume of investment but allocates it to the most productive projects. A negative interest rate increases volume, but allows investment in practically anything, increasing the probability that growth will be uneconomic. Shall we become hyper-Keynesians and push GDP growth to maintain full employment, even after growth has become uneconomic? Or shall we back off from growth and seek full employment by job sharing, distributive equity, and reallocation toward leisure and public goods?

Why would we allow growth to carry the macro-economy beyond the optimal scale? Because growth in GDP is considered the summum bonum, and it is heresy not to advocate increasing it. If increasing GDP makes us worse off we will not admit it, but will adapt to the experience of increased scarcity by pushing GDP growth further. Non-growth is viewed as stagnation, not as a sensible steady state adaptation to objective limits. Stimulating GDP growth by increasing consumption and investment, while cutting savings, is the only way that hyper-Keynesians can think of to serve the worthy goal of full employment. There really are other ways, and people really do need to save for security and old age, as well as for maintenance and replacement of the existing capital stock. Yet the Fed is being advised to penalize saving with a negative interest rate. The focus is on what the growth model requires, not on what people need.

A negative interest rate seems also to be the latest advice from Paul Krugman, who praises Summers insights. It is understandable from their viewpoint because in their vision the economy is not a subsystem, or if it is, it is infinitesimal relative to the total system. The economy can expand forever, either into the void or into a near infinite environment. It does not grow into a finite ecosphere, and therefore has no optimal scale relative to any constraining and sustaining environment. Its aggregate growth incurs no opportunity cost and can never be uneconomic. Unfortunately, this tacit assumption of the growth model is seriously wrong.

Larry Summers and other growth-obsessed economists are calling for negative interest rates.

|

Welcome to the full-world economy. In the old empty-world economy, assumed in the macro models of Summers and Krugman, growth always remains economic, so they advocate printing more and more dollars to expand the economy to take over ever more of the unemployed sources and sinks of the ecosystem. If a temporary liquidity trap or zero lower bound on interest rates keeps the new money from being spent, then low or even negative monetary interest rates will open the spending spigot. The empty world assumption guarantees that the newly expanded production will always be worth more than the natural wealth it displaces. But what may well have been true in yesterdays empty world is no longer true in todays full world.

This is an upsetting prospect for growth economists growth is required for full employment, but growth now makes us collectively poorer. Without growth we would have to cure poverty by redistributing wealth and stabilizing population, two political anathemas, and could only finance investment by reducing present consumption, a third anathema. There remains the microeconomic policy of reallocating the same GDP to a more efficient mix of products by internalizing external costs (getting prices right). While this certainly should be done, it is not macroeconomic growth as pursued by the Fed.

These painful choices could be avoided if only we were richer. So lets just focus on getting richer. How? By growing the aggregate GDP, of course! What? You repeat that GDP growth is now uneconomic? That cannot possibly be right, they say. OK, that is an empirical question. Lets separate costs from benefits in the existing GDP accounts, and develop more inclusive measures of each, and then see which grows more as GDP grows. This has been done (ISEW, GPI, Ecological Footprint), and results support the uneconomic growth view. If growth economists think these studies were done badly they should do them better rather than ignore the issue.

The leftover Keynesians are correct in pointing out that there is unemployed labor and capital. But natural resources are fully employed, indeed overexploited, and the limiting factor in the full world is natural resources, not labor or capital as used to be the case in the empty world. Some growth economists think that the world is still empty. Others think there is no limiting factor that capital is a good substitute for natural resources. This is wrong, as Nicholas Georgescu-Roegen has shown long ago. Capital funds and natural resource flows are complements, not substitutes, and the one in short supply is limiting. Increasing a non-limiting factor doesnt help. Growth economists should know this.

Although the growthists think quantitative easing will stimulate demand they are disappointed, even in terms of their own model, because the banks, who are supposed to lend the new money, encounter a lack of bankable projects, to use World Bank terminology. This of course should be expected in the new era of uneconomic growth. The new money, rather than calling forth new wealth by employing all these hypothetical idle resources from the empty world era, simply bids up existing asset prices in the full world. Most asset prices are not counted in the consumer price index, (not to mention exclusion of food and energy) so economists unconvincingly claim that quantitative easing has not been inflationary, and therefore they can keep doing it. And even if it causes some inflation, that would help make the interest rate negative.

Aside from needed electronic transaction balances, people would not keep money in the bank if the interest rate were negative. To make them do so, the alternative of cash would basically have to be eliminated, and all money would be electronic bank deposits. This intensifies central bank control, and the specter of bail-ins (confiscations of deposits) as occurred in Cyprus. Even as distrust of money increases, people will not immediately revert to barter, in spite of negative interest rates. Barter is so inconvenient that money remains more efficient even if it loses value at a rapid rate, as we have seen in several hyperinflations. But transactions balances will be minimized, and speculative and store-of value-balances will be diverted to real estate, gold, works of art, tulip bulbs, Bitcoins, and beanie babies, creating speculative bubbles. But not to worry, say Summers and Krugman, bubbles are a necessary, if regrettable, means to boost spending and growth in the era of newly recognized negative natural interest rates and still unrecognized uneconomic growth.

A bright silver lining to this cloud of confusion is that the recognition of a negative natural interest rate may be the prelude to recognition of the underlying uneconomic growth as its cause. For sure this has not yet happened because so far the negative natural interest rate is seen as a reason to push growth with a negative monetary interest rate, rather than as a signal that growth has become a losing game. But such a realization is a reasonable hope. Perhaps a step in this direction is Summers suggestion that the old Alvin Hansen thesis of secular stagnation might deserve a new look.

The logic that suggests negative interest also suggests negative wages as a further means of increasing investment by lowering costs. To maintain full employment via GDP growth, not only must the interest rate now be negative, but wages should become negative as well. No one yet advocates negative wages because subsistence provides an inconvenient lower positive bound below which workers die. On this other side of the looking glass the logic of uneconomic growth pushes us in the direction of a negative natural wage, just as with a negative natural rate of interest. So we artificially lower the wage costs to job creators by subsidizing below-subsistence wages with food stamps, housing subsidies, and unpaid internships. Negative interest rates also subsidize investment in job-replacing capital equipment, further lowering wages. Negative interest rates, and below-subsistence wages, further subsidize the uneconomic growth that gave rise to them in the first place.

The leftover Keynesians tell us, reasonably enough, that paying people to dig holes in the ground and then fill them up, is better than leaving them unemployed with no income. But paying people to deplete and pollute the Creation on which our lives and welfare ultimately depend, in order to expand the macro-economy beyond its optimal or even sustainable scale, is surely worse than just giving them a minimum income, and some leisure time, in exchange for doing no harm.

An artificial monetary rate of interest forced down by quantitative easing to equal a negative natural rate of interest resulting from uneconomic growth is not a solution. It is just baling wire and duct tape. But it is all that even our best and brightest economists can come up with as long as they are imprisoned in the empty world growth model. The way out of this trap is to recognize that the growth era is over, and that instead of forcing growth into uneconomic territory we must seek to maintain a steady-state economy at something approximating the optimal scale. Since we have overshot the optimal scale of the macro-economy, this will require a period of retrenchment to a reduced level, accompanied by much more equal sharing, frugality, and efficiency. Sharing means putting limits on the range of inequality that we permit; it has huge moral and social benefits, even if politically difficult. Frugality means using less resource throughput; it results in less depletion and pollution and more recycling and efficiency. Efficiency means squeezing more life-support and want-satisfaction from a given throughput by technological advance and by improvement in our ethical priorities. Economists need to replace the Keynesian-neoclassical growth synthesis with a new version of the classical stationary state.

|

ABOUT THE AUTHOR

Herman Daly has received numerous significant awards (e.g., the Right Livelihood Award and the NCSE Lifetime Achievement Award) that recognize the value of his ideas for making this world a better place. For decades, he has been an inspiration to students of economics and public policy how often do you see students lining up at the end of the semester to have their professor sign their textbooks?

Over his career, Herman has taken a courageous stance, swimming upstream against the currents of conventional economic thought. Not content to bequeath his ideas on economic development solely to the academic realm, he did time at the World Bank to change policies in the real world. He also has written books that are popular with citizens around the world.

Its a rare combination indeed to have keen insight, kindness, razor-sharp analytical skill, wit, amazing capacity for work, humility, and an uncanny way with words all rolled up into one human being. Its a good thing, too the planet needs Herman Daly. His books, lectures, papers, and essays (including the ones he writes for this blog!) are filled with ingredients for cooking up a better economy and better lives.

ABOUT THE CENTER FOR THE ADVANCEMENT OF THE STEADY STATE ECONOMY

The Center for the Advancement of the Steady State Economy (CASSE) is a research group on economic sustainability located in Arlington, Virginia, USA. The mission of CASSE is "to advance the steady state economy, with stabilized population and consumption, as a policy goal with widespread public support." The CASSE website provides many additional research resources on economic growth, degrowth, and post-growth. For example:

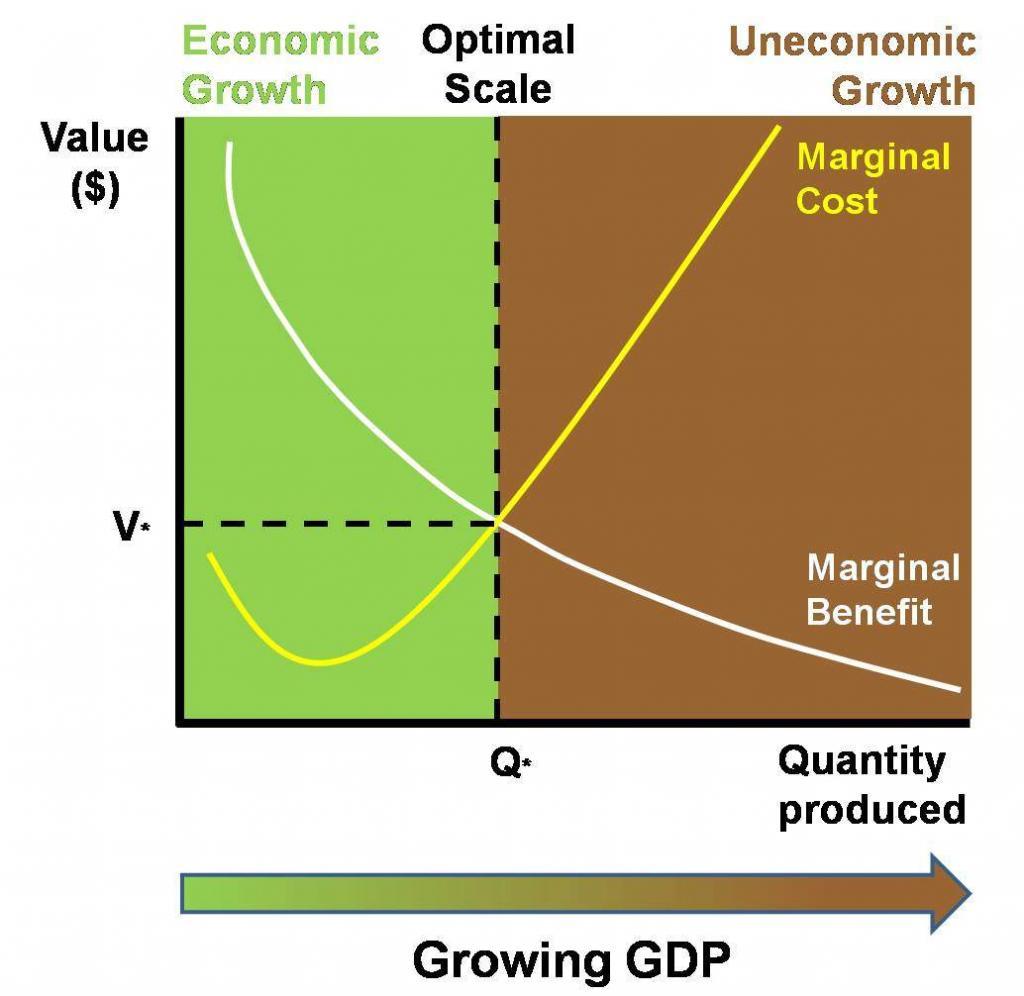

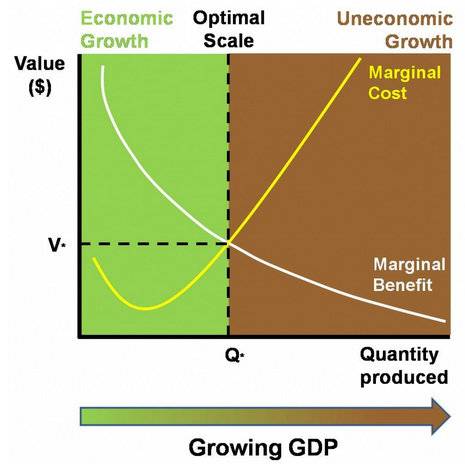

The following chart captures the basic rationales for the steady-state economy:

"Marginal cost refers to the cost of producing one more unit of a good or service. Marginal benefit is the benefit gained from one more unit. This graph shows the marginal costs and benefits of GDP growth. Costs tend to rise and benefits tend to decrease for each additional unit of growth. We should stop growing GDP, therefore, when marginal costs are exactly equal to marginal benefits. If costs are less than benefits, then GDP growth is economic (the green part of the graph). When costs rise above benefits, GDP growth is uneconomic (the brown part)."

|

Additional articles on the application of the fundamental steady-state economy concept to specifc issues can be found in the

The Daly News. The following is a list of recently published articles:

Steady Statesmanship Goes Global,

by Jon Rosales, The Daly News, 17 June 2013

Full Employment Versus Jobless Growth, Herman Daly, The Daly News, 15 July 2013

Entropia: Life Beyond Industrial Civilisation,

Samuel Alexander, The Daly News, 1 August 2013

Fixing Food and Farming with a True-Cost Economy, Brent Blackwelder, The Daly News, 6 August 2013

The End of the Age of Extraction, Brent Blackwelder, The Daly News, 2 September 2013.

Approaching a Steady State Economy, Part 1 Getting Around, Rob Dietz, The Daly News, 9 September 2013

Approaching a Steady State Economy, Part 2 Clean Clothes, Rob Dietz, The Daly News, 16 September 2013

Growth and Laissez-faire, Herman Daly, The Daly News, 23 September 2013.

Unlimited Competition Is Not Sustainable, Gunnar Rundgren, The Daly News, 30 September 2013.

Insanity Reigns at the World Bank, Brent Blackwelder, The Daly News, 14 October 2013.

A Question of Scarcity, Andrew Fanning, The Daly News, 21 October 2013.

How Many People Can a State Sustain?, George Plumb, The Daly News, 4 November 2013.

The Five Dumbest Things Youll Hear About Sustainability, Brian Czech, The Daly News, 12 November 2013.

Top 5 Threats to the Worlds Beaches (and a Systemic Solution), Brent Blackwelder, The Daly News, 18 November 2013.

The Hidden Door: Mindful Sufficiency as an Alternative to Extinction, Mark Burch, The Daly News, 16 December 2013.

Voluntary Simplicity and the Steady-State Economy, Mark Burch, The Daly News, 7 January 2014.

|

|Back to TITLE|

Page 1

Page 2

Page 3

Page 4

Page 5

Page 6

Page 7

Page 8

Page 9

Supplement 1

Supplement 2

Supplement 3

Supplement 4

Supplement 5

Supplement 6

PelicanWeb Home Page

|

|

|

|

"Nature is the art of God."

Dante Alighieri (12651321)

|

|

Page 3

|

|

FREE SUBSCRIPTION

|

![[groups_small]](groups_small.gif)

|

Subscribe to the

Mother Pelican Journal

via the Solidarity-Sustainability Group

Enter your email address:

|

|

|

|