Financial analysis relies heavily on exponential thinking

Let us say that you have the opportunity to receive 1000 Euros every year from today and for perpetuity. How much would you be ready to pay for it right now? The job of financial analysts is generally to answer that type of question by comparing costs and revenues today with costs and revenues expected in the future. It is assumed that anyone prefers to receive a sum of money now because waiting is regarded both as a cost and a risk.

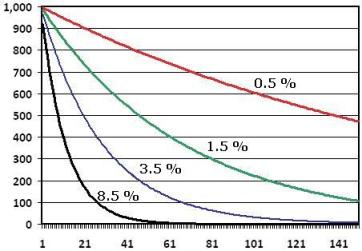

Annual present value of an allowance of 1000 Euros/year depending on the discount rate (200 first years). Photo credits: G Emin, A Damodaran

|

The cost of time and risk is usually taken into account through a discount rate (r). This rate expresses by how much you think that the value of 100 Euros received in the future is lower than the value of 100 Euros today. This is usually an annually-compounded rate, meaning that year 2 is worth r % less than year 1, and year 3 is worth r % less than year 2. However, compounding is exponential. Einstein once said: Compound interest is the eighth wonder of the world. The graph on energy consumption illustrates this idea and why it is unrealistic for example to think that we can achieve the growth rates of the last 60 years in the coming decades. This is also an issue for economic growth.

|

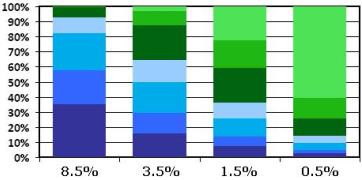

There are 7 colours from dark blue to light green, which respectively correspond to:

- % of value in years 1-5

- % of value in years 6-10

- % of value in years 11-20

- % of value in years 21-30

- % of value in years 31-60

- % of value in years 61-100

- % of value after year 100

|

Total present value of an allowance of 1000 Euros/year for perpetuity depending on the discount rate.

Photo Credits: G Emin, A Damodaran.

The exponential dimension of compounding is particularly important in financial analysis given that the conventional cost of equity (for listed companies) reached about 9% in the total market as of January 2012 (Damodaran, 1/12). The cost of debt was significantly lower at around 3.5% (after tax) because lenders are considered to take less risk than investors who own the company. However, the average cost of capital (taking debt into account) remained high at 7% (lower at c.4% for water utilities but higher at c.11.5% for advertising). Moreover, the return on equity of the total market (net income/book value of equity) reached c.11.5% as of January 2012 (Damodaran, 1/12).

Some very concrete consequences on the depreciation of the future

What do these numbers mean concretely? If I am an equity investor applying a 9% discount rate, it means that receiving 100 Euros in one year has for me the same present value as receiving 91 Euros right now. To put it in another way, it means that I will invest my money only if I expect an annual return of at least 9%. And this return is exponential!

As a result, conventional discount rates make it very difficult to think within a long-term perspective (see more details in the graphs). With a discount rate of 9% I should not agree to pay more than 11111 Euros to acquire an allowance of 1000 Euros per year for perpetuity, and the 20 first years would account for more than 80% of the total value of this allowance (while eternity less the 20 first years would account for the remaining 20%!). Of course the 9% rate takes into account a risk of not receiving the money as expected. Applying a high discount rate can, thus, be a way to be cautious in the short-term. However, high discount rates also tend to make us too short-sighted to analyse long-term risks correctly. Even less risky discount rates make long-term thinking difficult, as for example if we apply the average long-term rates of the US Treasury (c.3.5% in 2011 and c.4.5% over 2000-2011).

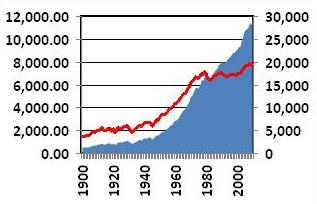

WORLD ENERGY CONSUMPTION 1900-2010

BLUE AREA - World primary energy consumption (Mtoe, lhs), CAGR 1950-2010: 3.3%

RED CURVE - World primary energy consumption per capita (kWh/person, rhs), CAGR 1950-2010: 1.6%

|

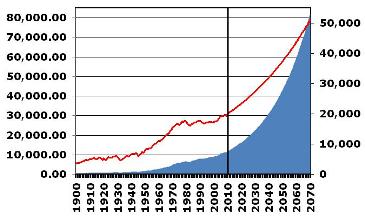

WORLD ENERGY CONSUMPTION 1900-2070

BLUE AREA - World primary energy consumption (Mtoe, lhs), CAGR 1950-2010: 3.3%

RED CURVE - World primary energy consumption per capita (kWh/person, rhs), CAGR 1950-2010: 1.6%

It is unrealistic to apply 1950-2010 compound annual growth rates to 2010-70 energy consumption. Photo Credits: Etemad & Luciani, US EIA, The Shift Project, UN, Angus Maddison

|

This significant impact of discounting has obvious consequences on how finance can look at climate change and energy issues. Energy resources are limited, which has significant economic consequences. However, if our discount rates tell us that financial costs projected for the next decades have almost no value, we may not see the rationality of making sacrifices for the future, instead of using as much energy as possible to boost immediate profits.

Climate change has also many consequences in the long-term as, for example, CO2 emissions have an atmospheric lifetime of 5-200 years. Of course it would not be enough to decrease discount rates. The modelling of discounted cash-flows itself must be improved through the integration of negative externalities in costs, as for example with a carbon tax.

And what about philosophy and religion?

Todays financial analysis should better take long-term risks into account. If only because, unlike us, future generations do not weight present revenues more than their future revenues.

Moreover, interest rates have often been regarded with caution throughout history (in the face of problems such as usury or greed), notably by the Jews of the Old Testament, ancient Greek philosphers, Christians and Muslims. In the Old Testament, the Bible speaks against interest rates in several places, as in Deuteronomy 23:19: You shall not charge interest to your brother interest on money or food or anything that is lent out at interest. Aristotle condemned the creation of money from money itself, and the canon law of the Catholic Church forbade lending money with interest until 1830. In Islam, interest remains prohibited although Islamic banking allows Muslims to develop some financial activities. It remains that our modern economic system was partly developed against intuitions that can be found in the three main monotheisms, as well as other sources.

To conclude, we should promote caution today in the face of unrealistic and sometimes disastrous dreams of exponential growth. We should also commit to the principle of gratuitousness and the logic of gift as an expression of fraternity (Caritas in Veritate, 2009). And not only in our lives but also at some level in commercial relationships. Lower interest and discount rates appear, thus, to be both a necessity of reason and a duty of justice. This may prove challenging but Jesus called us to a very challenging approach to lending in the Beatitudes: And if you lend to those from whom you hope to receive back, what credit is that to you? For even sinners lend to sinners to receive as much back. But love your enemies, do good, and lend, hoping for nothing in return (

). (Luke 6:34-35).

References

Damodaran Online

US Energy Information Administration Independent Statistics & Analysis

The Shift Project

United Nations

The Groningen Growth and Development Centre

Guillaume Emin is an SRI (Socially Responsible Investing) analyst and lives in Brussels, Belgium. You may get in touch with him via email: g.emin@hotmail.fr.

![[groups_small]](groups_small.gif)