|

China ended its rare earths embargo of the West last week, with

shipments resuming to Japan, the United States, and Europe after a

speech by Secretary of State Clinton raised the diplomatic stakes.

The ban ended as it began, quietly and without official notification.

The question now is whether the resumption of trade will lull the

developed world back into dependence, or whether the whole affair really

was, as Clinton described, a "wake-up call."

In many ways the embargo itself was a sideshow for two larger

disputesthe long-simmering maritime feud between China and Japan, and a

newer, fresher conflict that seems to be emerging with the developed

world over high-tech employment.

Beijing's use of its rare earths as a diplomatic cudgel was an

absurdly flawed tactic, but it brings this new conflict into clearer

definition. China's true challenge to the Westindeed, its winning

strategycan be found in its ambitious modernization goals this coming

decade. Set out in obscure committee directives and benign national

policy choices, these are its best-laid plans.

The following incident, unrelated to the embargo firestorm, is

instructive on this larger issue. On October 19, one day after an

important Chinese Communist Party plenary session had meted out the

nation's trajectory for the next five years, a leak from the Ministry of

Commerce indicated that export quotas for rare earth elements (REEs)

would be 30 percent lower in 2011. The Ministry report also mentioned that exports might be outlawed entirely in the coming decade.

How this outlawing of exports (or even the quotas themselves) squares

with the WTO precepts signed by Beijing in its 2000 accession agreement

was not discussed. Because China controls 95 percent of all REE

mining, the ban would hit Western manufacturers hard. The story was

picked up by the Associated Press. The leak was then immediately denied

the next day, but the fact that it emerged the day after the United

States launched a probe into Chinese subsidies of its green industry and

following a pivotal CCP meeting on future energy security is suggestive.

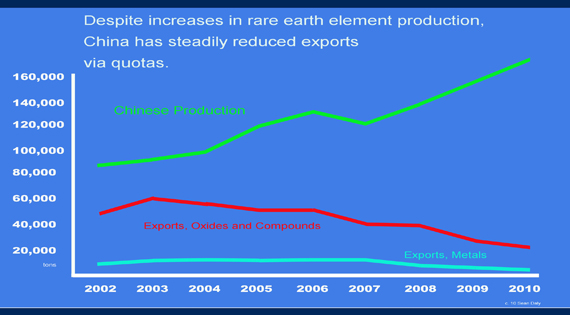

Indeed, such a reduction doesn't deviate from the trend: Foreign

exports have been tightening for seven years. China in July slashed its

late 2010 export quota by 72 percent, arguing the country needs to

protect its supplies for the future. Shipments would be capped at 8,000

metric tons, down from nearly 28,500 tons for the same period in 2009.

As the state-sponsored People's Daily made clear

in discussing the leaked report: "No one is entitled to criticize

China over this because this is an affair absolutely within China's

sovereignty."

Long the topic of metal speculators, the rare earths issue has

received copious press lately precisely because it intersects so many of

the great debates, anxieties, and aspirations of our time. As Beijing

seeks to cut off the world with a series of stringent quotas, those

cherished notions about free trade and an employment-enhancing "green

economy" are facing the tough reality of mercantilism, sourcing

monopolies, and an obscure world of technology metals that are rather

hard to mine cleanly.

There is a growing recognition that an emerging China might not

simply need a dignified "place at the table" and then always be a

progressive player on global agendas. In fact, as I wrote

earlier this year, China might behave more like the United Statesa

hungry, solipsistic nation, capable of fierce unilateralist tendencies.

Threading through various PRC policy discussions and governmental

white papers, a general consensus appears: The next decade offers China a

historic "window of opportunity" to focus on solving its big domestic

needs while also lifting the nation to technological parity with the

West. Beijing's obsession with its own modernization will likely shock

the developed world in the coming years, as all calls for free trade and

"fair play" are met with indifference or suspicion.

The recent rare earth embargoes of Japan and United States appear to confirm this point.

The "Informal" Embargo

The world certainly got a bit less "Friedman flat"

last month when Beijing swung to hot, coercive diplomacy following the

September 7 arrest of one of its fishing boat captains near the Senkaku

Islands.

Some flare up of nationalist sensitivities was to be expected, yet it

is still astonishing how quickly the crisis cascaded into every aspect

of Sino-Japanese relations. Following the arrest by the Japanese coast

guard, China canceled cultural exchanges, dropped tourism, and tabled

all energy plans. It arrested four Japanese nationals on trumped-up

spying charges. It spoke ominously of economic consequences, and within

a week all exports of rare earth elements to Japan mysteriously ceased.

Ordered by Chinese customs officials, this "informal" embargo of

neodymium and other metals aimed to wobble the Nikkei's high-tech

manufacturers.

Faced with questions at a conference on October 3, Wen Jiabao pointed

to the overzealous patriotism of individual exporters and declared that

shipments would quickly resume. But they did not.

Indeed, the unspoken halt to all shipments spread to other developed markets within two weeks. On October 19, the New York Times reported

that Chinese customs officials imposed restrictions on REEs bound for

the United States and Europe hours after a top Chinese official

denounced an American probe into Chinese subsidies. The restrictions

are explained now as a policy of heightened diligence. As Chinese

embassy spokesperson Wang Baodong described in a recent email:

With stricter export mechanism gradually in place,

outbound shipments to other countries might understandably begin to feel

the effect. But I don't see any link between China's reasonable rare

earth export control policy and the irrational U.S. decision of

protectionist nature to investigate China's clean energy industries.

Despite Wen's comments on October 3, the Japanese embargo stayed in

place for 26 more days, ending without any official acknowledgment on

October 29. Shipments to the United States and Europe also resumed that

day.

Whereas the developed world saw these trade bans as retaliatory,

Beijing soon presented them as a healthy approach to smuggling problems

amid necessary industry consolidation. The argument was that many of the

exporters had simply exhausted their quotas for the year and that the

lax environmental regulation that had allowed for pell-mell increases in

mining had to be curbed.

Ultimately both sides are right. The bans were clearly retaliatory;

China is concerned about its supply. But the rift in perspectives on

the issue suggests a new era may be taking shape: a bumpy

"deglobalizing" period when the developed world must question the wisdom

of trade dependence on China and cope with its inward focus.

Grand Plans for a Green China

The October CCP plenary session hammered out an ambitious plan. It

offers up a tough new energy agenda for the country, with a 1520

percent reduction in energy intensity over five years and a 4045

percent reduction in carbon emissions by 2020. It is a plan that can

only be met with a massive investment in "green" technology, which now

often depends on rare earth elements.

Rare earth metals are used extensively in the latest wind turbines

and electric cars. Traditional wind turbines have gearboxes that are

prone to break down. The new neodymium-iron-boron magnet generators have

far fewer moving parts and are therefore less costly to service in

extreme offshore locations. They are quickly becoming the turbine of

choice.

Similarly, each Toyota Prius hybrid uses 1 kilogram of neodymium in

its electric motor magnets, and about 10 kilograms of lanthanum in its

batteries. Those amounts will only go up as the car's power train

evolves for more efficiency.

Credit: Sean Daly (CC)

Earlier this year, China declared a national goal of reaching an

annual production rate of 1 million electric cars. Metals expert Jack

Lifton estimates

that this feat will require a staggering 1,000 metric tons of lanthanum

per year. Beijing is also aiming for 330 GW of wind turbine energy by

2020. Lifton suggests that this ten-year project will absorb some

59,000 metric tons of neodymium, 1,000 tons of terbium, and 3,000 tons

of dysprosium.

Producing all those green products is going to require a lot of rare earths.

The "Win-Win" Scenario

How will China maintain decent prices for the domestic companies it

has tapped to build its green future? It will control prices, curb

exports, and combat illegal mining. On July 10, 2010, China's Ministry

of Commerce declared full state intervention in the industry:

- All REE prices will be set by the central government, with a national price set each month.

- All REE mining companies will be consolidated by the state into 35 conglomerates.

- Exports for 2010 were to drop to 40 percent of 2009 levels.

Prices spiked for all rare earths following this action, with

neodymium outside of China quadrupling to $80,000 per ton. It sells at

half that inside the country.

On October 18, the Secretary General of the Chinese rare earths

industry association suggested that in-China use will soar from 75,000

tons per year today to 130,000 tons in five years. This is why foreign

exports may be reduced further anddenials asideexports of the "rarer"

rare earth elements might be outlawed altogether.

Developed countries were already squirming under recent Chinese

development strategies. Beijing started to reduce export quotas as

early as 2003. Though actual Chinese REE production climbed 60 percent

from 2003 to 2008, its exports to other countries during that period

dropped 50 percent.

Credit: Sean Daly (CC)

Why reduce exports,

especially when they fetch higher prices for the miners? China appears

to be implementing a nationalist agenda that does several things

simultaneously. By pressuring foreign companies to relocate factories,

with lower in-China sourcing costs as the lure, Beijing hopes to absorb

innovation and expand into those attractive industries. The move also

strengthens China's high-tech "national champions," which can produce at

even lower input costs than their Asian neighbors and mop up domestic

demand. China thus leverages its REE monopoly to climb up the

manufacturing chain, creating the magnets and value-added technologies

that require rare earths.

These "national champions" in the green and high-tech fields will

enhance employment at home, and their products will reduce pollution and

energy usage within China. They will also sell well in emerging

economies, further marginalizing the developed world's high-tech

manufacturers. The strategy produces a "guided market" virtuous circle.

The End of an Era

So how should the developed world react to reduced exports? These

new controls will draw down existing stockpiles and ultimately affect

high-tech pricing. According to Dudley Kingsnorth, executive director of Industrial Minerals Company of Australia:

First, the quotas are less than "rest of the world"

demand this year, which I did not believe would occur until 2011.

Second, if this trend continues, world supply will not be able to meet

the shortfall for several years. In the near future, the shortfall will

be met by a drawdown of stockpiles.

Prices are already up significantly this year for most rare earths.

Lanthanum has doubled since July following China's intervention. The

price of dysprosium in China has gone from $50 per kilogram in 2005 to

$290 per kilogram this October, with that number often double outside

the country.

The West is being asked to source its own rare earths. But it might

not yet understand just how much higher those prices will go, having

historically experienced a pricing environment that can only be

understood as an anomaly. In a recent report,

the strategic consultancy firm STRATFOR analyzed the pricing of rare

earths over the past three decades and concluded that the West has been

quite oblivious to how abnormally cheap the metals were during the last

20 years due to China's unregulated mining.

Yes, total disregard for occupational safety and environmental impact

allowed for low-cost REEs worldwide. Pictures of Baotou miners often

show them caked in mud laced with thorium and uranium.

But the STRATFOR report makes another very interesting point, one

rarely discussed. It suggests that Chinese state loans to mining

operationswhich were focused on "social stability through full

employment" and not profitabilitygave the world decades of supply:

The REE industrylike many other heavy or extractive

industrieswas targeted with massive levels of subsidized loans in the

mid-1980s.

Production rates increased by an annual average of 40

percent in the 1980s. They doubled in the first half of the 1990s, and

then doubled again with a big increase in output just as the world

tipped into recession in 2000.

World prices predictably plunged, by an average of 95 percent

compared to their pre-China averages. The consultancy firm computes

that if world prices were to go back to 1980s levels (and a non-Chinese

supply), the developed world would be seeing a vastly different cost

structure for many now pervasive productsincluding computer drives,

compact fluorescent bulbs, even those Apple earphones.

Take, for example, the Toyota Prius battery system. Its rare earths

components were responsible for a mere 0.9 percent of the car's cost in

2009. That percentage has increased to 2.9 percent due to higher

lanthanum costs this year, and that cost would increase further still to

15.2 percent if pre-China prices were applied.

Manage and Control

Last week, in a sign of growing concern, a collection of 35 business

groups from the United States, Europe, and Asia sent an open letter

asking officials at the G-20 meeting in Seoul to try to resolve the

issue of rare earths exports and their free trade. Unfortunately, it is

unclear what kind of real leverage over Beijing there is on this issue.

Tellingly, on the same day, the chemical giant W. R. Grace bid to

secure non-Chinese supplies. It tapped a new U.S. miner ramping up

initial processing in California, promising to buy 75 percent of all

lanthanum produced.

At the Asia-Europe Summit in Brussels last month, Wen Jiabao made a statement

on rare earths: "What we are pursuing is the sustainable development of

rare earths, which is necessary to meet our national needsand also the

needs of the world." Wen, a trained geologist, went on to say that it

was "necessary" to "manage and control" the rare earths market.

About the Author: Sean Daly is an analyst and development consultant based in New York. He has written extensively on Asian economic development, exploring issues as diverse as Chinese urbanization, CMI multilateral currency swap arrangements, energy geopolitics in Kazakhstan, and Singapores high-tech water industry. He was educated at Columbia University and NYU and was a visiting lecturer at Princeton University from 2006 to 2009. His equity approach is to chart the broader demographic issues of globalization and find sectors, companies, or resources that are likely to benefit from emerging macro-trends. Opportunities are further refined through fundamental analysis and some basic quantitative techniques. Technical indicators are used exhaustively to determine tactical entry or exit points.

|Back to ABSTRACT|

Page 1

Page 2

Page 3

Page 4

Page 5

Page 6

Page 7

Page 8

Page 9

Supplement 1

Supplement 2

Supplement 3

Supplement 4

PelicanWeb Home Page

|

![[groups_small]](groups_small.gif)